by: Detroit News

Average long-term U.S. mortgage rate dips to 6.17%, its lowest level in more than a year

by: People

")

by: Action News Jax

Jacksonville invites public to learn about Shipyards West Park Project at November 6 open house

by: KOB 4

Americans staying put: US home turnover rate at lowest level in decades as housing slump drags on

by: Sporting News

by: SheKnows

Andrew's New Home After Royal Lodge Eviction Has Been Revealed but Where Will Sarah Ferguson Live?

by: Billboard

by: Berkshire Eagle

by: Milwaukee Journal Sentinel

Recent million-dollar Wisconsin home sales include Tudor-style house, lakefront condo

Average long-term U.S. mortgage rate dips to 6.17%, its lowest level in more than a year

Detroit News

Detroit News

Why the spike?

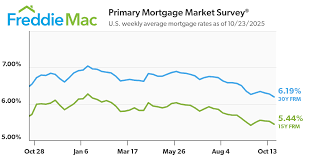

The surge follows a sequence of policy signals from the Federal Reserve that has been tightening its monetary policy to combat stubborn inflation. The Fed’s 2025‑10‑12 meeting released a statement confirming that it would continue to raise the federal funds rate by 25 bps, with a possibility of an additional hike in December. Treasury officials explained that the increase in short‑term rates cascades into the long‑term Treasury yields, which in turn lift mortgage rates, as most residential loans are anchored to the 10‑year Treasury yield.

The article quotes Dr. Emily Tan, chief economist at the Mortgage Bankers Association (MBA), who noted that “the 10‑year Treasury yield’s jump from 3.52 % to 3.88 % last week has a direct impact on mortgage pricing.” She added that the MBA’s monthly survey of mortgage originators indicated a 12 % decline in new loan applications in September, a trend that is likely to continue if rates remain elevated.

In addition to Fed policy, the piece references a recent Beige Book release that highlighted weaker demand in the housing market and “increased caution among home‑buyers, especially those with tighter budgets.” The Beige Book’s comments were cited as evidence that rising rates have already dampened the appetite for new home purchases, even in traditionally hot markets like Detroit and the Midwest.

The ripple effects on borrowers

Higher mortgage rates mean higher monthly payments, a fact that is already altering the landscape for prospective buyers. The Detroit News article interviewed two families who had postponed their move into a newly built subdivision in Southfield. “We had to put a hold on it because we’re looking at $2,600 a month versus $2,400,” said Maria Lopez, a project manager with a 30‑year fixed plan. “We’re now looking at a 15‑year mortgage, but the interest cost is still a concern.”

The shift toward adjustable‑rate mortgages (ARMs) was highlighted as a strategic move by many borrowers. The article points to a surge in applications for 5/1‑ARM products, which feature a lower initial rate for five years before adjusting annually. However, experts caution that while ARMs can lower short‑term payments, they expose borrowers to the risk of rate increases in the future.

For homeowners considering refinancing, the article underscores that the cost‑benefit equation has flipped. While many had locked in low rates in 2023, the current environment makes refinancing less attractive unless the borrower can secure a substantial rate reduction or a longer amortization period. The Detroit News article cites a recent case where a homeowner had to pay nearly $5,000 in closing costs to refinance, only to end up with a higher monthly payment than the original loan.

Impact on the market and the broader economy

Real‑estate analysts in the story argue that the sustained rise in rates could stall the housing market’s recovery after the pandemic‑era boom. The article references a study from the National Association of Realtors (NAR) which projects a 4 % decline in home sales by the end of 2025, a fall that could be tied directly to affordability concerns.

Lenders are also tightening underwriting standards. The Detroit News piece quotes a loan officer at Wells Fargo who said that “the bank’s risk‑adjusted pricing model now requires higher credit scores and larger down payments.” The result is a widening of the affordability gap, especially for first‑time buyers and low‑to‑moderate income households.

On the supply side, the article points to a slowdown in new construction. A contractor from the Michigan Association of Builders, whose office was featured in the piece, reported a 9 % drop in residential building permits over the past quarter. He attributed the decline to the uncertainty around financing costs, which, in turn, leads developers to hold off on large‑scale projects.

What the future holds

The article concludes with a look at what might lie ahead. It notes that while the Federal Reserve could pause rates for the next quarter, the prevailing economic data suggests that inflation is still stubborn. In a segment covering the Fed’s upcoming meeting, the piece quotes a speech from Jerome Powell, who said that “the central bank remains committed to keeping the economy on a sustainable path.”

Mortgage economists predict that rates could climb to 6.9 % by mid‑2026, a figure that would further tighten the housing market. However, some analysts point to the possibility that the Fed might signal a pivot toward rate cuts if the economy shows signs of a slowdown. “It’s a delicate balance,” said Dr. Tan. “The Fed has to weigh the risk of overheating against the risk of a recession.”

The Detroit News article offers a comprehensive snapshot of the forces shaping mortgage rates in late 2025. With the Fed’s policy moves, Treasury yields, and broader economic indicators all feeding into the numbers, the story provides readers with a clear picture of why rates have spiked and what that means for anyone looking to buy or refinance a home in the months ahead.

Read the Full Detroit News Article at:

https://www.detroitnews.com/story/business/2025/10/30/mortgage-rates/86989172007/

Like: 👍

on: Tue, Oct 07th 2025

by: Fortune

Current ARM mortgage rates report for Oct. 7, 2025 | Fortune

on: Tue, Sep 09th 2025

by: WGME

on: Tue, Sep 30th 2025

by: Fortune

Current mortgage rates report for Sept. 30, 2025: Rates mostly stay put | Fortune

on: Wed, Sep 10th 2025

by: Fortune

Current ARM mortgage rates report for Sept. 10, 2025 | Fortune

on: Wed, Sep 10th 2025

by: Fortune

Current mortgage rates report for Sept. 10, 2025: Rates continue downward trend | Fortune

on: Wed, Aug 13th 2025

by: Fortune

30-Year Fixed Mortgage Rates Slip to 5.85% as Fed Holds Inflation in Check

on: Sun, Aug 03rd 2025

by: fingerlakes1

Mortgage Rates Dip Slightly This Week, Offering Small Relief

on: Thu, Jul 31st 2025

by: Fortune

Mortgage Rates Dip Slightly in Late July 2025: What Homebuyers Need to Know

on: Wed, Jul 30th 2025

by: Local 12 WKRC Cincinnati

Mortgage Rates Plummet to Lowest Levels in Months, Boosting Homebuyer Hope

on: Thu, Jul 24th 2025

by: CNET

Mortgage Predictions With Fed Cutson Hold Where Do Rates Go From Here

on: Thu, Oct 23rd 2025

by: Channel 3000

on: Wed, Oct 22nd 2025

by: Local 12 WKRC Cincinnati