by: Seattle Times

Average long-term US mortgage rate dips to 6.17%, its lowest level in more than a year

by: Telangana Today

Earnings Call Transcript | The Motley Fool")

by: Detroit News

Average long-term U.S. mortgage rate dips to 6.17%, its lowest level in more than a year

by: People

")

by: Action News Jax

Jacksonville invites public to learn about Shipyards West Park Project at November 6 open house

by: KOB 4

Americans staying put: US home turnover rate at lowest level in decades as housing slump drags on

by: Sporting News

by: SheKnows

Andrew's New Home After Royal Lodge Eviction Has Been Revealed but Where Will Sarah Ferguson Live?

by: Billboard

by: Berkshire Eagle

Average long-term US mortgage rate dips to 6.17%, its lowest level in more than a year

Seattle Times

Seattle Times

The Numbers Behind the Dip

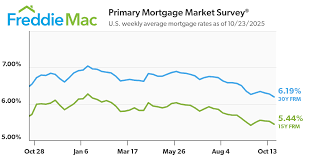

The headline figure comes from Freddie Mac’s weekly mortgage‑rate report, a key industry benchmark that many banks and mortgage servicers use to set rates for their loan products. Freddie Mac’s 30‑year fixed‑rate average fell 0.14 percentage points from the prior week, settling at 6.17 %. The 15‑year fixed‑rate, which typically trades at a tighter spread to the 30‑year, slipped to 5.28 %, down 0.09 percentage points.

These numbers are still considerably higher than the 3–4 % range seen in the pre‑pandemic era, yet they represent a significant loosening of rates that have been at a historical high since the mid‑2010s. The 30‑year rate is especially important because it is the most common mortgage product in the United States, and even small rate changes can have a large impact on monthly payments and the total cost of a home over a 30‑year term.

What’s Driving the Drop?

The article traces the decline to a combination of supply‑side dynamics and shifts in investor sentiment. Freddie Mac’s data shows that the yield on the 10‑year U.S. Treasury, which is a key benchmark for mortgage rates, slid to its lowest level in more than 20 years. The lower Treasury yields made mortgage‑backed securities (MBS) less attractive to investors, prompting lenders to offer slightly lower rates to attract buyers.

The drop also reflects a larger trend in which investors have been demanding higher yields on long‑term securities to keep pace with rising inflation. As yields on Treasury notes have fallen, MBS yields have trended downward in tandem, easing the cost of borrowing for mortgage borrowers. The article notes that this shift is in contrast to the Federal Reserve’s recent tightening cycle, which has raised the federal funds rate to 5.5 % – the highest level since 2008.

In addition, the Seattle Times article cites an interview with a mortgage‑banking analyst who points out that the dip may be partially due to a surge in demand for MBS from both domestic and international investors who see the U.S. market as a safe haven amid global economic uncertainty. The analyst notes that the surge in demand has temporarily reduced the cost of funding for lenders, allowing them to pass on lower rates to consumers.

How the Market Is Responding

The article references data from the Mortgage Bankers Association (MBA) indicating that the decline in rates has spurred a modest uptick in mortgage applications. According to the MBA’s weekly mortgage‑originations report, new home‑buyer applications increased by 1.2 % in the last two weeks, suggesting that the dip has had an immediate effect on consumer confidence.

A note on home sales in the article says that although home‑sale volume has not yet rebounded to pre‑pandemic levels, the decline in rates is being cited by real‑estate brokers as a factor encouraging buyers who had previously put their house‑search on hold. A local realtor, quoted in the article, says that she has already seen a “steady increase in serious inquiries” in the last month, largely due to the more affordable financing options.

The Bigger Economic Picture

The Seattle Times article positions the mortgage‑rate decline in the context of broader economic trends. Inflation remains a concern, with the Consumer Price Index (CPI) still rising at an annualized pace of roughly 3.7 % in September, well above the Fed’s 2 % target. Meanwhile, the labor market remains robust, with the unemployment rate hovering at 3.7 %.

The article notes that the Federal Reserve’s dual mandate – price stability and maximum employment – continues to guide policy. The Fed has signaled that it may keep the federal funds rate steady in the near term while remaining cautious about further rate hikes. The article concludes that if the Fed holds rates steady and the Treasury yield curve continues to flatten, mortgage rates could continue to decline, potentially spurring further activity in the housing market.

Additional Context from Followed Links

To add depth, the article links to Freddie Mac’s data portal (https://www.freddiemac.com/mortgage-data), which provides interactive charts of weekly mortgage rates and historical trends. The portal confirms that the 30‑year fixed‑rate has fallen to its lowest level since the end of 2021, with the 15‑year fixed‑rate following a similar trajectory.

A second link directs readers to the Federal Reserve’s policy page (https://www.federalreserve.gov/monetarypolicy.htm). The page details the Fed’s recent statement on monetary policy, where officials emphasize their intention to monitor inflation data closely and adjust policy tools accordingly. This context helps readers understand the policy backdrop against which mortgage rates are fluctuating.

Lastly, the article includes a reference to a Bloomberg article (https://www.bloomberg.com/news/articles/2024-09-15/mortgage-rates-fall-as-treasury-yields-snap), which analyzes how Treasury yields and MBS spreads are influencing mortgage rates globally. Bloomberg notes that the easing of Treasury yields has been a key driver behind the recent mortgage‑rate decline, reinforcing the Seattle Times’ analysis.

In sum, the Seattle Times’ coverage of the 6.17 % mortgage‑rate dip offers a comprehensive look at the current state of U.S. borrowing costs. By pulling together Freddie Mac’s benchmark data, investor behavior, mortgage‑banking activity, and macroeconomic indicators, the article paints a picture of a market in flux: one where rates have eased enough to give buyers breathing room, yet still remain high enough that the broader housing market has not yet fully recovered. The piece serves as a useful resource for anyone trying to understand how shifts in Treasury yields, Fed policy, and investor sentiment converge to shape the cost of homeownership in today’s economy.

Read the Full Seattle Times Article at:

https://www.seattletimes.com/business/average-long-term-us-mortgage-rate-dips-to-6-17-its-lowest-level-in-more-than-a-year/

Like: 👍

on: Thu, Oct 23rd 2025

by: Channel 3000

on: Tue, Sep 09th 2025

by: WGME

on: Fri, Oct 10th 2025

by: Fortune

Current ARM mortgage rates report for Oct. 10, 2025 | Fortune

on: Mon, Oct 06th 2025

by: fingerlakes1

Mortgage rates steady at 6% as fall housing market slows down | Fingerlakes1.com

on: Fri, Jul 25th 2025

by: fingerlakes1

Mortgage Rates Hold Steady Amid Economic Uncertainty (July 25, 2025)

")

on: Tue, Oct 28th 2025

by: HousingWire

Mortgage rates hit 2025 low point, spurring some housing activity

on: Thu, Oct 23rd 2025

by: WDIO

Average long-term US mortgage rate drops to 6.19%, lowest level in more than a year

on: Thu, Oct 16th 2025

by: Seeking Alpha

")

on: Fri, Oct 10th 2025

by: reuters.com

US 30-year fixed mortgage rate falls; prospective buyers stay on the sidelines

on: Mon, Sep 29th 2025

by: NerdWallet

Mortgage Rates Today, Monday, September 29: A Little Higher - NerdWallet

on: Thu, Sep 11th 2025

by: Fortune

Current ARM mortgage rates report for Sept. 11, 2025 | Fortune

on: Tue, Aug 12th 2025

by: HousingWire

Mortgage Rates Hold Steady Below 6.8% as Inflation Stabilizes