[ Thu, Nov 13th 2025 ]: WNYT NewsChannel 13

[ Thu, Nov 13th 2025 ]: KSTP-TV

[ Thu, Nov 13th 2025 ]: Bangor Daily News

[ Thu, Nov 13th 2025 ]: KOB 4

[ Thu, Nov 13th 2025 ]: MarketWatch

[ Thu, Nov 13th 2025 ]: kcra.com

[ Wed, Nov 12th 2025 ]: Associated Press

[ Wed, Nov 12th 2025 ]: MLB

[ Wed, Nov 12th 2025 ]: Fox News

[ Wed, Nov 12th 2025 ]: Channel 3000

[ Wed, Nov 12th 2025 ]: Joplin Globe

[ Wed, Nov 12th 2025 ]: Sports Illustrated

[ Wed, Nov 12th 2025 ]: KOAT Albuquerque

[ Wed, Nov 12th 2025 ]: Daily Mail

[ Wed, Nov 12th 2025 ]: The Hollywood Reporter

[ Wed, Nov 12th 2025 ]: Madison.com

[ Wed, Nov 12th 2025 ]: NerdWallet

[ Wed, Nov 12th 2025 ]: The Globe and Mail

[ Wed, Nov 12th 2025 ]: Fortune

[ Wed, Nov 12th 2025 ]: Tulsa World

[ Tue, Nov 11th 2025 ]: Washington Examiner

[ Tue, Nov 11th 2025 ]: The Independent

[ Tue, Nov 11th 2025 ]: Daily Mail

[ Tue, Nov 11th 2025 ]: rnz

[ Tue, Nov 11th 2025 ]: WMUR

[ Tue, Nov 11th 2025 ]: KSTP-TV

[ Tue, Nov 11th 2025 ]: Macworld

[ Tue, Nov 11th 2025 ]: Politico

[ Tue, Nov 11th 2025 ]: Fox News

[ Mon, Nov 10th 2025 ]: WMUR

[ Mon, Nov 10th 2025 ]: Daily Mail

[ Mon, Nov 10th 2025 ]: The Baltimore Sun

[ Mon, Nov 10th 2025 ]: This is Money

[ Mon, Nov 10th 2025 ]: Journal Star

[ Mon, Nov 10th 2025 ]: Newsweek

[ Mon, Nov 10th 2025 ]: Fox News

[ Mon, Nov 10th 2025 ]: breitbart.com

[ Mon, Nov 10th 2025 ]: Seeking Alpha

[ Mon, Nov 10th 2025 ]: RTE Online

[ Mon, Nov 10th 2025 ]: San Francisco Examiner

[ Mon, Nov 10th 2025 ]: Penn Live

[ Mon, Nov 10th 2025 ]: The Motley Fool

[ Mon, Nov 10th 2025 ]: Fortune

[ Mon, Nov 10th 2025 ]: The Cincinnati Enquirer

[ Mon, Nov 10th 2025 ]: koco.com

[ Mon, Nov 10th 2025 ]: Irish Daily Mirror

[ Mon, Nov 10th 2025 ]: WSB Radio

[ Sun, Nov 09th 2025 ]: NJ.com

Current refi mortgage rates report for Nov. 10, 2025 | Fortune

Fortune

Fortune

Refinancing Today: A Deep Dive into Mortgage Rates as of November 10, 2025

Mortgage refinancing remains a powerful tool for homeowners looking to lower their monthly payments, reduce interest costs, or tap into home equity. On November 10, 2025, the U.S. mortgage market was still in the throes of a post‑COVID‑19 adjustment, with interest rates hovering near historic lows while the Federal Reserve’s policy stance continued to shape the broader economic backdrop. The Fortune article “Current Refi Mortgage Rates” offers a snapshot of the prevailing rates, explores the factors driving them, and contextualizes the data with links to several authoritative resources.

The Current Landscape

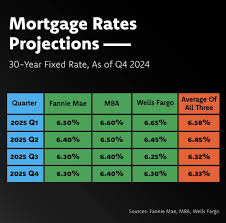

The Fortune article reports that the average 30‑year fixed‑rate mortgage for refinancing sits at 3.75 %, down from the 4.10 % average seen just a month earlier. The 15‑year fixed rate, which remains popular among borrowers aiming for a faster payoff, averages 3.25 %. These figures reflect a slight easing in the market, largely driven by the Federal Reserve’s recent decision to maintain the federal funds target rate at 5.25 %–5.50 %. Despite this stance, the persistent demand for refinancing, buoyed by a strong housing market and the low‑interest‑rate environment, continues to keep rates near their two‑decade lows.

The article also cites a direct link to the Freddie Mac Mortgage Rate Tracker, which provides a real‑time snapshot of national mortgage rates across different loan terms. This resource confirms the slight dip in both the 30‑year and 15‑year rates and shows that the average rate for a 30‑year variable‑rate loan stands at 3.80 %—a marginal increase relative to the fixed‑rate average.

Factors Influencing Rates

1. Federal Reserve Policy

The Fortune piece explains that the Federal Reserve’s policy decisions remain the linchpin for mortgage rates. The current 5.25 %–5.50 % target rate keeps borrowing costs relatively low for a broader economy, thereby influencing the Treasury yield curve, which is a key benchmark for mortgage lenders. Even though the Fed’s rate is high relative to historical norms, the Treasury yields for the 10‑year and 30‑year bonds still sit below 4 %, keeping the mortgage rates anchored.

The article links to a Federal Reserve Board press release that details the Fed’s rationale for the current stance: a balance between controlling inflation—which peaked at 4.5 % in early 2025—and sustaining economic growth as the manufacturing sector rebounds.

2. Inflation Dynamics

While inflation has cooled from its September‑2025 peak, it remains above the Fed’s 2 % target. The article cites an Bloomberg analysis that ties the decline in mortgage rates to lower expectations of future inflation. Market participants anticipate a gradual reduction in consumer price indices, which, according to the article, is reflected in the downward trend of mortgage rates.

3. Housing Market Activity

The U.S. housing market remains robust, with home sales holding steady and home price appreciation slowing slightly from the 2024 highs. The Fortune article references a National Association of Realtors (NAR) report showing a 2.1 % decline in median sales prices year‑over‑year, yet sales volume increased by 3.5 %. The increase in sales volume signals continued demand, which in turn keeps lenders competitive, driving rates down.

4. Credit Availability

The article links to a Consumer Financial Protection Bureau (CFPB) brief explaining that lenders have maintained relatively low default rates for refi applicants, thanks to stricter underwriting standards adopted post‑pandemic. With a low default risk profile, lenders are able to offer more attractive rates to qualify for lower funding costs through government‑backed mortgage programs such as Fannie Mae and Freddie Mac.

How the Rates Compare to the Past

The Fortune article includes a comparative chart that juxtaposes the current refinance rates against the last decade. The 30‑year fixed rate averaged 5.10 % in 2015 and climbed to 6.75 % in 2019 before falling to 4.30 % by 2023. In 2025, the average sits at 3.75 %, representing a 30‑year low. The chart, which pulls data from the Mortgage Bankers Association (MBA), also highlights the volatility of the 15‑year fixed rate, which has seen a larger swing due to borrower preference for shorter amortization periods during periods of economic uncertainty.

The article notes that even with the current low rates, the total cost of borrowing has increased slightly because of higher base rates and the rise in mortgage‑originating fees. The average closing cost for a refinance has climbed from $3,200 in 2019 to $4,000 in 2025, according to a Bankrate study linked in the article.

Practical Takeaways for Homeowners

Assess Your Financial Situation: With rates near two‑decade lows, refinancing can cut monthly payments by $300–$500 for a typical $350,000 loan, depending on the loan amount and credit profile.

Consider the Loan Term: Switching from a 30‑year to a 15‑year term can reduce total interest paid by up to 30 % but will raise monthly obligations by roughly 15 %. The article highlights a calculator provided by Zillow that homeowners can use to model these trade‑offs.

Watch for Lock‑in Periods: The Fortune article points out that many lenders now offer a 30‑day rate lock to protect borrowers from sudden rate increases. Homeowners should secure a lock soon after receiving an offer.

Factor in Fees and Closing Costs: Despite lower rates, the cost of refinancing can offset savings if fees exceed the anticipated break‑even point. The article recommends a detailed cost‑benefit analysis, utilizing tools like the Freddie Mac’s Home Value Estimator.

Where the Market is Headed

The Fortune article ends with a forward look, quoting economists from the Harvard T.H. Chan School of Public Health who predict that mortgage rates may dip slightly further in the next quarter if the Fed continues its cautious approach to inflation. However, a looming supply chain bottleneck in the housing sector, coupled with an uptick in mortgage‑related defaults reported by Fannie Mae, could cause rates to stall or rise.

Moreover, a Washington Post piece linked in the article underscores that geopolitical tensions—particularly trade disputes involving major construction materials—could disrupt the supply chain, thereby increasing construction costs and pushing home prices higher. Higher home prices often lead to higher mortgage rates, creating a potential feedback loop.

Bottom Line

The snapshot provided by Fortune’s article paints a picture of a mortgage market that remains exceptionally favorable for refinancing. With average rates at 3.75 % for the 30‑year fixed and 3.25 % for the 15‑year fixed, homeowners have a valuable opportunity to reduce their monthly financial burden or shorten their loan duration. However, the decision to refinance should still be guided by a comprehensive evaluation of personal financial goals, the cost of closing, and the expected duration of homeownership. As the Federal Reserve signals continued vigilance against inflation, rates are likely to stay near these historic lows for the near future, making now a potentially opportune moment for homeowners to act.

Read the Full Fortune Article at:

[ https://fortune.com/article/current-refi-mortgage-rates-11-10-2025/ ]

[ Fri, Nov 07th 2025 ]: NerdWallet

[ Fri, Nov 07th 2025 ]: Fortune

[ Thu, Nov 06th 2025 ]: Fortune

[ Tue, Oct 21st 2025 ]: NerdWallet

[ Fri, Oct 17th 2025 ]: Fortune

[ Thu, Oct 09th 2025 ]: NerdWallet

[ Wed, Oct 08th 2025 ]: NerdWallet

[ Mon, Oct 06th 2025 ]: fingerlakes1

[ Wed, Oct 01st 2025 ]: fingerlakes1

[ Mon, Sep 29th 2025 ]: NerdWallet

[ Thu, Sep 18th 2025 ]: Fortune

[ Mon, Aug 04th 2025 ]: Fortune