")

Current mortgage rates report for Nov. 25, 2025 | Fortune

Fortune

FortuneLocale: UNITED STATES

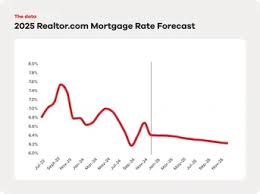

Thursday, March 12th, 2026 - Mortgage rates have continued their downward trajectory, reaching unprecedented lows not seen in over fourteen years. As of today, the average 30-year fixed mortgage rate has fallen to a remarkable 2.95%, a significant drop from the 3.5% reported in late 2025 and sparking a renewed wave of activity in the housing market. This sustained decline is prompting a massive surge in both home purchases and refinance applications, injecting fresh momentum into the overall economy.

From Dovish Signals to Record Lows: A Deep Dive

The initial dip in rates, first observed in late 2025, was largely attributed to a pivot in the Federal Reserve's monetary policy. After a period of measured rate increases aimed at curbing inflation, the Fed signaled a more accommodating stance, hinting at potential rate cuts to stimulate economic growth. This shift was fueled by slowing economic indicators and a perceived easing of inflationary pressures. However, the rates have fallen further than initially anticipated.

"The initial expectation of Fed easing was the catalyst, but several other factors have contributed to this prolonged and substantial decline," explains Dr. Anya Sharma, Chief Economist at Global Finance Analytics. "Global economic uncertainty, particularly geopolitical tensions and concerns over international trade, have driven investors towards the safety of U.S. Treasury bonds. This increased demand has pushed bond yields down dramatically, directly impacting mortgage rates. We're also seeing a flattening of the yield curve, further contributing to lower long-term rates."

Dr. Sharma also points to a significant increase in mortgage-backed security (MBS) purchases by the Federal Reserve, a tactic used to further lower rates and provide liquidity to the market. This quantitative easing strategy has amplified the downward pressure on mortgage rates.

Refinance Boom Continues - and Evolves

The refinance market is experiencing an unprecedented boom. The Mortgage Bankers Association (MBA) reported a 212% increase in refinance applications compared to the same period last year. While initial applications focused on simple rate-and-term refinances - lowering monthly payments or shortening loan terms - a new trend is emerging: cash-out refinances. Homeowners, flush with equity gained from recent property value appreciation, are increasingly tapping into that equity for home renovations, debt consolidation, and even investment opportunities.

"We're seeing a shift in the type of refinance applications," says David Lee, a senior loan officer at Stellar Home Loans. "Initially, it was all about saving money on monthly payments. Now, more and more homeowners are looking to use their home equity to fund other life goals. This is a clear sign of increased consumer confidence."

New Home Construction Surges, Addressing Supply Concerns

The lower rates are not only impacting existing homeowners; they're also fueling a surge in new home construction. Builders, encouraged by increased demand and lower financing costs, are breaking ground on new projects at the fastest pace in over a decade. This is a welcome development, as the housing market has been plagued by a chronic shortage of inventory for years. The increased supply, while not yet fully realized, is expected to help moderate price increases in the long run. However, materials costs remain a concern, with ongoing supply chain disruptions potentially limiting the pace of construction.

What Lies Ahead? Navigating the Volatility

While the current environment is highly favorable for borrowers, experts caution that rates are unlikely to remain at these historically low levels indefinitely. The Federal Reserve is expected to begin tapering its MBS purchases in the coming months, which could put upward pressure on rates. However, the timing and pace of tapering remain uncertain, dependent on economic data and evolving global conditions.

"We anticipate moderate increases in rates over the next six to twelve months," predicts Dr. Sharma. "But we don't expect a sharp spike. The Fed is likely to proceed cautiously, balancing the need to control inflation with the desire to support economic growth. Homeowners considering a refinance or purchase should act now to lock in rates before they start to rise."

Furthermore, the upcoming presidential election in late 2026 adds another layer of uncertainty. The economic policies of the next administration could have a significant impact on the housing market and mortgage rates. Homebuyers and homeowners are advised to stay informed and consult with financial professionals to make informed decisions.

Read the Full Fortune Article at:

https://fortune.com/article/current-mortgage-rates-11-25-2025/

Fortune

on: Sat, Feb 28th

by: Fortune

on: Sat, Feb 28th

by: Fortune

on: Sat, Feb 28th

by: NBC Los Angeles

on: Thu, Feb 26th

by: The Boston Globe

on: Wed, Feb 25th

by: Fortune

on: Tue, Feb 24th

by: Newsweek

on: Tue, Feb 10th

by: Fortune

on: Fri, Feb 06th

by: Fortune

on: Mon, Feb 02nd

by: WSFA

on: Fri, Feb 27th

by: NBC Washington

on: Fri, Feb 27th

by: Fortune

on: Thu, Feb 26th

by: Fortune