by: Investopedia

by: Business Today

Affordable housing norms may see overhaul, says Housing minister Manohar Lal Khattar - BusinessToday

by: fingerlakes1

Mortgage rates dip slightly, but housing market shows signs of stress | Fingerlakes1.com

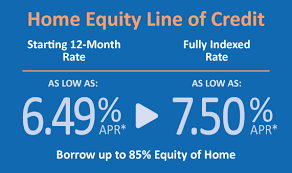

Current Heloc Rates--And How to Get the Lowest Ones

Wall Street Journal

Wall Street Journal

HELOC Rates in 2024: A 500‑Plus‑Word Summary of the Wall Street Journal’s Latest Analysis

The Wall Street Journal’s latest “Buyside” feature on home‑equity lines of credit (HELOCs) offers a detailed look at how borrowers can navigate the current rate environment, what factors lenders use to set rates, and how a HELOC compares to other financing options. Below is a comprehensive recap of the article’s key points, including insights from the many links the WSJ weaves into the story.

1. What a HELOC Is and Why It Matters

The article begins by laying the groundwork for readers who may be new to the concept. A HELOC is a revolving credit line that uses a homeowner’s equity as collateral. Unlike a traditional mortgage, the borrowing amount is not set at the outset; instead, the borrower can draw from the line up to an agreed‑upon limit, repaying as needed. Because of this flexibility, many homeowners use HELOCs for home improvements, debt consolidation, or unexpected expenses.

The feature stresses that HELOCs are typically variable‑rate products, meaning the interest rate can change over the life of the line of credit. This is a critical point for anyone considering a HELOC, because the “starting” rate can shift with market conditions.

2. The Current Rate Landscape

Using data from Bankrate’s HELOC rate tracker (https://www.bankrate.com/mortgages/heloc-rates/), the WSJ reports that, as of August 2024, the average introductory rate for a HELOC is 7.2 %. The median rate sits just under 7 %. These figures reflect a modest rise from the 6.8 % average seen in the previous quarter, but the article notes that rates are still roughly 1.5–2.0 % higher than the rates on fixed‑rate mortgages for the same loan term.

The piece points out that the spread between a HELOC and a fixed mortgage is partly due to the “margin” lenders add on top of the prime rate or the 10‑year Treasury yield. Most banks use a margin of 2.0–2.5 %, whereas the margin on a 30‑year fixed mortgage might be closer to 1.0–1.5 %. Because of this, a borrower might get a HELOC at 7.2 % and a 30‑year fixed mortgage at 5.8 %—the difference is real.

3. The Variables That Shape Your Rate

The WSJ’s analysis dives into the five key factors lenders weigh when pricing a HELOC:

| Factor | How It Impacts Rate |

|---|---|

| Credit Score | Higher scores (e.g., 740+) can secure a lower margin, sometimes 0.25 % less. |

| Debt‑to‑Income (DTI) Ratio | A lower DTI (≤ 36 %) can reduce risk and lead to a better rate. |

| Loan‑to‑Value (LTV) Ratio | Lenders prefer LTV ≤ 80 %; higher LTV can add 0.5–1.0 % to the rate. |

| Lender Competition | Strong competition (e.g., credit unions) can drive rates down. |

| Economic Environment | Fed policy and Treasury yields set the baseline for prime; any shift can ripple through HELOC rates. |

The article also links to the Federal Reserve’s FOMC minutes (https://www.federalreserve.gov/monetarypolicy.htm) for readers who want to understand how the Fed’s policy decisions impact prime rates and, consequently, HELOC pricing.

4. Lender Comparisons: Banks, Credit Unions, and Online Lenders

The WSJ walks readers through the current “field” of lenders:

- Big‑Name Banks: Wells Fargo, JPMorgan Chase, and Citibank still offer HELOCs, but their rates tend to sit on the higher end of the spectrum (7.5–8.0 %) due to higher operational costs.

- Credit Unions: These nonprofit institutions often provide rates 0.25–0.5 % lower than big banks. The WSJ notes that some credit unions also offer “no‑closing‑cost” options.

- Online Lenders: Companies like SoFi and Rocket Mortgage frequently run promotional rates (as low as 6.8 %) for new applicants, though terms can vary in terms of the length of the introductory period and the discount on the margin.

The article suggests using comparison tools such as NerdWallet’s HELOC comparison page (https://www.nerdwallet.com/best-mortgages/heloc) to see a side‑by‑side view of rates, fees, and repayment terms.

5. The Tax Angle: Deductibility and Home‑Improvement Use

A significant point in the article is that, as of the 2018 tax reform, HELOC interest is only deductible if the funds are used for home‑improvement projects that add value, not for general debt consolidation or personal expenses. Readers can check the IRS’s guidelines on home‑improvement deductions (https://www.irs.gov/credits-deductions/individuals/home-improvement) for more detail. The WSJ emphasizes that this tax nuance should factor into the decision whether a HELOC is the right tool for a borrower.

6. Strategies to Secure a Lower Rate

The piece offers a “cheat sheet” of tactics for homebuyers who want the most favorable terms:

- Improve Your Credit: Even a 10‑point bump can shave 0.1–0.15 % off the margin.

- Shop Around: Rate comparisons can reveal up to a 0.5 % difference.

- Ask About Rate Caps: Some lenders cap the maximum rate (e.g., prime + 5 %) to protect against extreme volatility.

- Consider a “Rate Lock”: Locking a rate for 12–24 months can hedge against rising rates if you expect a rate hike in the near future.

- Choose a Fixed Portion: Many lenders offer a hybrid HELOC that lets you lock in a portion of the line at a fixed rate for the first few years.

- Maintain Low LTV: If you can reduce the loan amount (e.g., through a down payment), lenders often reward lower LTV with better rates.

The article warns, however, that the “lock” or “fixed” portions come at a premium, often costing 0.25–0.5 % more than a fully variable line.

7. Market Outlook: What’s Next for HELOC Rates?

The WSJ concludes by projecting the direction of HELOC rates in the coming months. With the Fed’s recent decision to keep the federal funds rate near 5.5 % and the 10‑year Treasury yield hovering around 4.0 %, the benchmark for HELOCs remains relatively high. The article notes that while the Fed may pause rate hikes for now, any shift upward could push HELOC rates above 8 % in the short term.

The piece also points to an often‑overlooked factor: housing market dynamics. As home prices moderate, the equity pool shrinks, which could reduce the demand for HELOCs and in turn lower rates for a brief period—though the article cautions that this effect is likely to be short‑lived.

Bottom Line

The Wall Street Journal’s in‑depth look at HELOC rates equips readers with the tools to understand their options and make data‑driven decisions. Key takeaways:

- Current rates hover around 7.2 %; rates are typically 1.5–2.0 % above fixed mortgage rates.

- Credit score, LTV, DTI, and the economic backdrop are the main drivers of pricing.

- Credit unions and online lenders often offer the best rates, but banks still have a role for those seeking specific perks or larger loan limits.

- Tax deductibility is limited to home‑improvement uses, so that may influence whether a HELOC is the right financial instrument.

- Strategic actions—improving credit, shopping, negotiating caps, and considering rate locks—can lower the final cost.

For anyone considering a HELOC, the WSJ recommends starting with a comparison tool, reviewing the lender’s rate‑cap and margin policies, and aligning the borrowing purpose with tax rules. With these insights and a careful assessment of the current market, borrowers can secure a rate that fits their budget and long‑term financial strategy.

Read the Full Wall Street Journal Article at:

https://www.wsj.com/buyside/personal-finance/mortgage/heloc-rates

Wall Street Journal

on: Wed, Jul 30th 2025

by: wjla

on: Sun, Aug 17th 2025

by: Fox 11 News

on: Fri, Aug 08th 2025

by: news4sanantonio

on: Thu, Jul 31st 2025

by: moneycontrol.com

on: Wed, Jul 30th 2025

by: Local 12 WKRC Cincinnati

Federal Reserve Rate Cuts Impact Home Equity Rates in July 2025

on: Fri, Jul 25th 2025

by: Wall Street Journal

on: Mon, Aug 25th 2025

by: fingerlakes1

MORTGAGE RATES TODAY: Housing market alarms going off | Fingerlakes1.com

on: Sat, Aug 23rd 2025

by: Local 12 WKRC Cincinnati

Home equity rates dip as hopes of a Fed September slash strengthen

on: Fri, Aug 22nd 2025

by: Fox 11 News

Beyond the Hammer: A Clear Look at Home Improvement Loans – Are They Right For You?

on: Mon, Aug 11th 2025

by: fingerlakes1

on: Sun, Aug 03rd 2025

by: Wall Street Journal

on: Sat, Aug 02nd 2025

by: Wall Street Journal