[ Fri, Feb 27th ]: The Courier-Journal

[ Fri, Feb 27th ]: NOLA.com

[ Fri, Feb 27th ]: OPB

[ Fri, Feb 27th ]: Seattle Times

[ Fri, Feb 27th ]: CNBC

[ Fri, Feb 27th ]: NBC 10 Philadelphia

[ Fri, Feb 27th ]: BBC

[ Fri, Feb 27th ]: ThePrint

[ Fri, Feb 27th ]: HELLO! Magazine

[ Fri, Feb 27th ]: rnz

[ Fri, Feb 27th ]: Wrestling News

[ Fri, Feb 27th ]: KTBS

[ Fri, Feb 27th ]: WMUR

[ Thu, Feb 26th ]: Los Angeles Times

[ Thu, Feb 26th ]: Seattle Times

[ Thu, Feb 26th ]: Birmingham Mail

[ Thu, Feb 26th ]: Asia One

[ Thu, Feb 26th ]: Houston Public Media

[ Thu, Feb 26th ]: Bangor Daily News

[ Thu, Feb 26th ]: The Globe and Mail

[ Thu, Feb 26th ]: NBC Washington

[ Thu, Feb 26th ]: Fox Business

[ Thu, Feb 26th ]: The Hans India

[ Thu, Feb 26th ]: Orlando Sentinel

[ Thu, Feb 26th ]: Washington Examiner

[ Thu, Feb 26th ]: The Hollywood Reporter

[ Thu, Feb 26th ]: National Hockey League

[ Thu, Feb 26th ]: CBS News

[ Thu, Feb 26th ]: Fortune

[ Thu, Feb 26th ]: The Boston Globe

[ Thu, Feb 26th ]: Deadline.com

[ Thu, Feb 26th ]: New York Post

[ Thu, Feb 26th ]: Associated Press

[ Thu, Feb 26th ]: 9NEWS

[ Thu, Feb 26th ]: NJ.com

[ Thu, Feb 26th ]: IndieWire

[ Thu, Feb 26th ]: Mediaite

[ Thu, Feb 26th ]: The New Indian Express

[ Thu, Feb 26th ]: WSB-TV

[ Thu, Feb 26th ]: MassLive

[ Thu, Feb 26th ]: Irish Daily Mirror

[ Thu, Feb 26th ]: The West Australian

[ Thu, Feb 26th ]: BBC

[ Thu, Feb 26th ]: dw

[ Thu, Feb 26th ]: Manchester Evening News

[ Thu, Feb 26th ]: Toronto Star

[ Thu, Feb 26th ]: Fox News

Mortgage Rates Surge to 7.09%, Threatening Housing Market

Locale: UNITED STATES

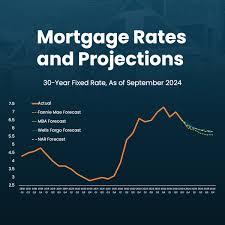

Jacksonville, FL - February 26th, 2026 - The American housing market is facing renewed headwinds as mortgage rates continue their upward trajectory, now averaging 7.09% for a 30-year fixed rate, as reported by Freddie Mac today. This marks the highest level in years, sending ripples of concern through potential homebuyers, real estate professionals, and economists alike. The rapid increase is not simply a statistical blip; it represents a fundamental shift in the affordability landscape, prompting a re-evaluation of budgets and purchasing power across the nation.

The jump from 6.81% just last week underscores the velocity of this change. While seemingly small, even a fractional increase translates to substantial differences in monthly mortgage payments and overall cost of homeownership. Rebecca Smith, a local prospective buyer, voiced the frustrations of many: "I've been pre-approved, I'm ready to buy, but I don't know if I can afford it anymore with these rates." Her story is becoming increasingly common, highlighting the growing barrier to entry for first-time homebuyers and those looking to move up the property ladder.

The Federal Reserve and the Fight Against Inflation

The driving forces behind these escalating rates are complex, but primarily stem from the ongoing battle against inflation and the Federal Reserve's monetary policy. As financial advisor John Miller explains, "They've been working to cool the economy, and one way to do that is to make borrowing more expensive." This cooling effect is intentional. The Fed aims to curb spending and investment by raising the cost of credit, including mortgages. The logic is that higher rates will decrease demand, bringing inflation down to the target rate of 2%.

However, the effectiveness of this strategy is being debated. While inflation has demonstrably slowed from its peak in 2022, it remains stubbornly above the Fed's target. This necessitates a delicate balancing act - raising rates enough to control inflation without triggering a significant recession. The current environment suggests the Fed is prioritizing inflation control, even at the risk of further dampening housing demand.

Impact on Sales and Inventory

The immediate impact of higher mortgage rates is already visible in slowing sales. While inventory levels remain relatively tight in many markets, the pace of transactions has noticeably decreased. Potential buyers are either postponing their purchases, seeking smaller or more affordable homes, or retreating from the market altogether. This cooling effect is particularly pronounced in previously "hot" markets that experienced rapid price appreciation during the pandemic.

Looking ahead, economists predict a continued moderation in home price growth, and potentially even price declines in certain regions. The extent of these declines will depend on several factors, including the duration of high interest rates, the overall health of the economy, and the level of housing inventory.

Shifting Strategies for Buyers and Sellers

For prospective homebuyers, the current environment demands a more cautious and strategic approach. Exploring adjustable-rate mortgages (ARMs), although carrying inherent risks, might offer a lower initial rate. However, buyers must carefully assess their risk tolerance and financial stability. Furthermore, down payment assistance programs and other affordability initiatives are becoming increasingly important resources. Negotiating with sellers on price and contingencies is also crucial.

Sellers, on the other hand, need to adjust their expectations. The days of multiple offers and bidding wars are largely over. Pricing homes competitively and making necessary repairs and upgrades to attract buyers are essential. Offering incentives such as closing cost assistance or rate buydowns can also help to overcome buyer hesitation.

Long-Term Outlook The long-term outlook for the housing market remains uncertain. Many experts believe that mortgage rates will eventually stabilize, but the timing and level of that stabilization are difficult to predict. A sustained decline in inflation and a shift in the Fed's monetary policy would likely lead to lower rates. However, geopolitical events and unexpected economic shocks could easily disrupt this trajectory.

The current situation represents a significant challenge for the U.S. housing market, but also an opportunity for adaptation and innovation. By understanding the underlying factors driving these changes and adjusting strategies accordingly, both buyers and sellers can navigate this complex landscape and achieve their housing goals.

Read the Full Action News Jax Article at:

https://www.actionnewsjax.com/news/business/average-us-long-term/SEFX5BQBSIZNLPMADV2EBFPWIQ/

[ Wed, Feb 25th ]: MarketWatch

[ Tue, Feb 24th ]: Fortune

[ Tue, Feb 24th ]: Newsweek

[ Mon, Feb 23rd ]: Fortune

[ Sun, Feb 22nd ]: Fortune

[ Fri, Feb 20th ]: Fortune

[ Thu, Feb 19th ]: wjla

[ Tue, Feb 10th ]: Fortune

[ Fri, Feb 06th ]: HousingWire

[ Thu, Feb 05th ]: WTOP News

[ Thu, Feb 05th ]: WTOP News

[ Mon, Feb 02nd ]: WSFA