[ Thu, Feb 26th ]: wjla

[ Thu, Feb 26th ]: IndieWire

[ Thu, Feb 26th ]: Motherly

[ Thu, Feb 26th ]: Mediaite

[ Thu, Feb 26th ]: The New Indian Express

[ Thu, Feb 26th ]: WSB-TV

[ Thu, Feb 26th ]: MassLive

[ Thu, Feb 26th ]: Irish Daily Mirror

[ Thu, Feb 26th ]: WFXR Roanoke

[ Thu, Feb 26th ]: The West Australian

[ Thu, Feb 26th ]: KUTV

[ Thu, Feb 26th ]: BBC

[ Thu, Feb 26th ]: news4sanantonio

[ Thu, Feb 26th ]: dw

[ Thu, Feb 26th ]: Manchester Evening News

[ Thu, Feb 26th ]: NY Post

[ Thu, Feb 26th ]: East Bay Times

[ Thu, Feb 26th ]: Toronto Star

[ Thu, Feb 26th ]: Fox News

[ Thu, Feb 26th ]: KARK

[ Thu, Feb 26th ]: The Independent

[ Wed, Feb 25th ]: TMJ4

[ Wed, Feb 25th ]: HousingWire

[ Wed, Feb 25th ]: KIRO-TV

[ Wed, Feb 25th ]: Robb Report

[ Wed, Feb 25th ]: abc13

[ Wed, Feb 25th ]: Fox News

[ Wed, Feb 25th ]: The Raw Story

[ Wed, Feb 25th ]: Fox 11 News

[ Wed, Feb 25th ]: Seeking Alpha

[ Wed, Feb 25th ]: MarketWatch

[ Wed, Feb 25th ]: The Independent

[ Wed, Feb 25th ]: FOX 5 Atlanta

[ Wed, Feb 25th ]: Fortune

[ Wed, Feb 25th ]: Daily Mail

[ Wed, Feb 25th ]: Cleveland.com

[ Wed, Feb 25th ]: Birmingham Mail

[ Wed, Feb 25th ]: WISH-TV

[ Wed, Feb 25th ]: 7NEWS

[ Wed, Feb 25th ]: The Center Square

[ Wed, Feb 25th ]: Billboard

[ Wed, Feb 25th ]: CBS News

[ Wed, Feb 25th ]: Daily Record

[ Wed, Feb 25th ]: Local 12 WKRC Cincinnati

[ Wed, Feb 25th ]: WSB Radio

[ Wed, Feb 25th ]: WTOP News

[ Wed, Feb 25th ]: The West Australian

[ Wed, Feb 25th ]: NBC Los Angeles

Housing Market: Rates Down, Prices Stuck

FOX 5 Atlanta

FOX 5 AtlantaLocale: UNITED STATES

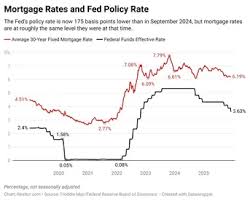

ATLANTA - February 25th, 2026 - The narrative surrounding the housing market is becoming increasingly complex. While the welcome decline in mortgage rates has sparked optimism amongst potential homebuyers, a significant drop in home prices appears unlikely - at least in the short term. This isn't a contradiction, but rather a consequence of a uniquely constrained market where falling rates are offset by stubbornly low inventory.

As of today, the average 30-year fixed mortgage rate stands at approximately 6.7%, a substantial decrease from the peaks experienced last year. Financial expert Jason Steele of Horizon Financial Planning notes, "This is genuinely good news for those looking to enter the market. Lower rates directly translate to lower monthly payments, boosting affordability and theoretically increasing purchasing power." He elaborates that this allows potential buyers to either borrow more for the same monthly outlay, or purchase a similar property for a slightly reduced amount in terms of monthly cost. However, the crucial distinction lies between affordability and actual price.

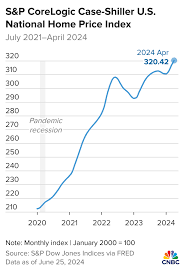

The core issue isn't affordability; it's availability. The housing supply remains critically low across much of the nation. Realtor Chris Eades, a leading agent with Atlanta Homes Group, explains, "We're simply not seeing a surge in homes coming onto the market. This lack of supply is the primary factor preventing prices from falling, despite the more favorable interest rate environment." The dynamic creates a strange paradox: rates are down, but prices remain elevated.

This situation is largely fueled by the 'rate lock-in' effect. Millions of homeowners secured historically low mortgage rates in the years preceding the recent rate hikes. These homeowners are understandably reluctant to sell their homes and subsequently purchase new properties at significantly higher rates. As Eades points out, "They're effectively trapped. They might want to upgrade or downsize, but the financial disincentive is too strong. They're comfortable where they are and unwilling to trade a 3% rate for a 6.7% rate, even if it means missing out on potential equity gains." This reluctance dramatically constricts the number of existing homes available for sale.

While the lower monthly payments are undoubtedly helpful, they haven't translated into substantial price reductions. Steele confirms, "The overall cost of buying a home - the actual price tag - hasn't experienced a drastic correction. The demand is still there, and with limited supply, prices are being held aloft." A simple illustration demonstrates the point: a $300,000 home with a 3% rate had a significantly lower monthly payment than the same home at 8%. Now, with rates around 6.7%, the payment has decreased from that peak, but the $300,000 price remains largely unchanged.

One bright spot in the landscape is new construction. Builders are responding to the demand, and we are witnessing a notable increase in housing starts. Steele highlights, "New home construction is accelerating. This will gradually alleviate the supply constraints, providing more options for buyers and potentially putting downward pressure on prices over time." However, Eades cautions that this relief won't be immediate. "Building takes time. Land development, permitting, construction... it's a lengthy process. It's going to take months, if not years, for the influx of new builds to significantly impact the overall market and really shift the supply-demand balance."

Experts predict a continued period of stagnation in housing prices. While a full-blown price crash is considered unlikely, significant price declines are not anticipated. Instead, the market is expected to remain competitive, with buyers still facing bidding wars and limited choices, particularly in desirable locations. The impact of regional economic factors will also play a key role. Areas with strong job growth and population influx will likely maintain higher prices, while those experiencing economic downturns may see more moderate adjustments.

For potential homebuyers, the current situation presents a mixed bag. Lower rates are a definite positive, but they need to be realistic about prices. Patience and a willingness to consider a wider range of locations and property types may be necessary to navigate this challenging market. The key takeaway: don't assume falling rates automatically mean cheaper houses. It's a far more nuanced picture.

Read the Full FOX 5 Atlanta Article at:

https://www.fox5atlanta.com/news/why-cheaper-home-loans-might-not-mean-cheaper-houses

[ Wed, Feb 18th ]: Newsweek

[ Fri, Feb 06th ]: WHIO

[ Fri, Feb 06th ]: Fortune

[ Thu, Feb 05th ]: Newsweek

[ Tue, Feb 03rd ]: Las Vegas Review-Journal

[ Sat, Jan 24th ]: Orange County Register

[ Wed, Jan 21st ]: CNBC

[ Tue, Jan 20th ]: The Oklahoman

[ Wed, Jan 14th ]: MarketWatch

[ Wed, Jan 07th ]: Newsweek

[ Fri, Dec 05th 2025 ]: The Spokesman-Review

[ Fri, Nov 21st 2025 ]: HousingWire