[ Thu, Feb 26th ]: Mediaite

[ Thu, Feb 26th ]: The New Indian Express

[ Thu, Feb 26th ]: WSB-TV

[ Thu, Feb 26th ]: MassLive

[ Thu, Feb 26th ]: Irish Daily Mirror

[ Thu, Feb 26th ]: WFXR Roanoke

[ Thu, Feb 26th ]: The West Australian

[ Thu, Feb 26th ]: KUTV

[ Thu, Feb 26th ]: BBC

[ Thu, Feb 26th ]: news4sanantonio

[ Thu, Feb 26th ]: dw

[ Thu, Feb 26th ]: Manchester Evening News

[ Thu, Feb 26th ]: NY Post

[ Thu, Feb 26th ]: East Bay Times

[ Thu, Feb 26th ]: Toronto Star

[ Thu, Feb 26th ]: Fox News

[ Thu, Feb 26th ]: KARK

[ Thu, Feb 26th ]: The Independent

[ Wed, Feb 25th ]: TMJ4

[ Wed, Feb 25th ]: news4sanantonio

[ Wed, Feb 25th ]: HousingWire

[ Wed, Feb 25th ]: KIRO-TV

[ Wed, Feb 25th ]: Robb Report

[ Wed, Feb 25th ]: abc13

[ Wed, Feb 25th ]: Fox News

[ Wed, Feb 25th ]: The Raw Story

[ Wed, Feb 25th ]: wjla

[ Wed, Feb 25th ]: Fox 11 News

[ Wed, Feb 25th ]: Seeking Alpha

[ Wed, Feb 25th ]: MarketWatch

[ Wed, Feb 25th ]: The Independent

[ Wed, Feb 25th ]: FOX 5 Atlanta

[ Wed, Feb 25th ]: WGME

[ Wed, Feb 25th ]: Fortune

[ Wed, Feb 25th ]: Daily Mail

[ Wed, Feb 25th ]: Cleveland.com

[ Wed, Feb 25th ]: Birmingham Mail

[ Wed, Feb 25th ]: WISH-TV

[ Wed, Feb 25th ]: 7NEWS

[ Wed, Feb 25th ]: The Center Square

[ Wed, Feb 25th ]: Billboard

[ Wed, Feb 25th ]: CBS News

[ Wed, Feb 25th ]: Daily Record

[ Wed, Feb 25th ]: Local 12 WKRC Cincinnati

[ Wed, Feb 25th ]: WSB Radio

[ Wed, Feb 25th ]: WTOP News

[ Wed, Feb 25th ]: The West Australian

[ Wed, Feb 25th ]: NBC Los Angeles

ARM Rates Hold Steady Near 7% - Is This the New Normal?

Fortune

FortuneLocale: UNITED STATES

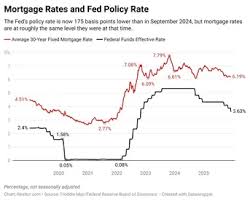

Wednesday, February 25th, 2026 - Adjustable-rate mortgage (ARM) rates continue to hold steady near the 7% mark, a level that feels increasingly entrenched as the new reality for the housing market. While many anticipated a swift correction following the aggressive interest rate hikes of the past two years, rates have proven remarkably persistent. This sustained elevation is dramatically reshaping the landscape for potential homebuyers and existing homeowners alike, prompting a critical question: is 7% the 'new normal' for ARM rates, or a temporary plateau before further adjustments?

As of today, the average 30-year ARM rate remains stubbornly around 7%, a significant jump from the historic lows experienced during the pandemic era. This stability, while offering a slight reprieve from the rapid increases of 2024, does little to alleviate the affordability crisis gripping the nation. The ripple effects are being felt across the entire housing ecosystem.

The Forces Behind the Persistence

The primary driver of these elevated rates remains the ongoing, albeit moderating, inflation. Although the Federal Reserve has signaled a potential pause in its rate-hiking cycle, the central bank remains committed to its 2% inflation target, and concerns about a resurgence of price increases continue to loom. The Fed's monetary policy, specifically adjustments to the federal funds rate, directly impacts borrowing costs, and the market is hypersensitive to any indications of future actions.

"The market is caught in a complex dance of anticipation," explains Sarah Chen, a senior economist at Financial Insights Group. "Investors are constantly reassessing the likelihood of future Fed moves, and that inherent uncertainty fuels volatility. It's not just about the current inflation number; it's about the expectation of future inflation."

Beyond inflation and Fed policy, broader economic factors are also at play. Geopolitical tensions, particularly ongoing conflicts and trade disruptions, contribute to supply chain issues and upward pressure on prices. Domestic economic resilience, while positive in many respects, also reduces the urgency for the Fed to aggressively cut rates. Strong employment numbers and continued consumer spending indicate a robust economy that isn't necessarily demanding lower borrowing costs.

A Cooling Housing Market and the Refinance Drought

The impact on the housing market has been palpable. Home sales have slowed considerably compared to the frenetic pace of 2021-2022. While inventory remains constrained in many areas, the reduced demand has begun to create a more balanced market. Sellers are increasingly forced to adjust their expectations and offer concessions to attract buyers. Perhaps the most striking consequence has been the near-total collapse of refinancing activity. With rates higher than those on most existing mortgages, the incentive to refinance has evaporated for all but a small segment of homeowners.

"The era of easy money is definitively over," notes David Miller, a real estate analyst at MarketWatch. "Prospective buyers are having to fundamentally recalibrate their budgets, considering significantly higher monthly payments. For many, the dream of homeownership is being pushed further out of reach."

Is 7% Here to Stay? The Experts Weigh In

The million-dollar question is whether the current 7% level represents a sustainable equilibrium, or merely a temporary pause before a further climb or, ultimately, a decline. Opinions among analysts are divided. Some believe that as inflation continues to cool and the Fed eventually begins to ease monetary policy, rates will gradually drift lower. However, they caution against expecting a swift return to the ultra-low rates of the past. Others maintain that persistent inflationary pressures, coupled with geopolitical risks, could keep rates elevated for an extended period.

Chen suggests a cautious outlook. "We could see a modest decline over the next six to twelve months, perhaps edging closer to the 6.5% range. But a substantial drop--anything below 6%--is unlikely unless we observe a significant and sustained improvement in the economic outlook. The Fed will be extremely cautious about cutting rates prematurely and risking a re-acceleration of inflation."

Miller leans towards the pessimistic side. "I anticipate rates remaining in this 6.5% to 7.5% range for the foreseeable future. The structural factors supporting inflation--global supply chain vulnerabilities, tight labor markets--are unlikely to resolve quickly. Homebuyers must prepare themselves for a higher cost of borrowing and adjust their expectations accordingly."

Resources for Monitoring Mortgage Rates:

- Bankrate: Provides daily updates on mortgage rates, calculators, and expert analysis.

- Freddie Mac: Offers the Primary Mortgage Market Survey (PMMS), a widely-followed benchmark for mortgage rates.

- Mortgage News Daily: Delivers real-time mortgage rate tracking and in-depth market commentary.

Read the Full Fortune Article at:

https://fortune.com/article/current-arm-mortgage-rates-01-26-2026/

[ Tue, Feb 24th ]: Fortune

[ Tue, Feb 24th ]: Newsweek

[ Mon, Feb 23rd ]: Fortune

[ Sun, Feb 22nd ]: Fortune

[ Fri, Feb 20th ]: Fortune

[ Tue, Feb 10th ]: Fortune

[ Fri, Feb 06th ]: Fortune

[ Fri, Feb 06th ]: Fortune

[ Thu, Feb 05th ]: WTOP News

[ Tue, Feb 03rd ]: Fortune

[ Mon, Feb 02nd ]: WSFA

[ Mon, Feb 02nd ]: Fortune