[ Tue, Feb 24th ]: Fortune

[ Tue, Feb 24th ]: News-Topic, Lenoir, N.C.

[ Tue, Feb 24th ]: Robb Report

[ Tue, Feb 24th ]: Detroit Free Press

[ Tue, Feb 24th ]: Reason.com

[ Tue, Feb 24th ]: 7News Miami

[ Tue, Feb 24th ]: Irish Examiner

[ Tue, Feb 24th ]: Fox News

[ Tue, Feb 24th ]: HousingWire

[ Tue, Feb 24th ]: Variety

[ Tue, Feb 24th ]: U.S. News & World Report

[ Tue, Feb 24th ]: WVUE FOX 8 News

[ Tue, Feb 24th ]: Insider

[ Tue, Feb 24th ]: Fox Sports

[ Tue, Feb 24th ]: NBC Connecticut

[ Tue, Feb 24th ]: Lehigh Valley Live

[ Tue, Feb 24th ]: Liverpool Echo

[ Tue, Feb 24th ]: Sporting News

[ Tue, Feb 24th ]: WTKR

[ Tue, Feb 24th ]: Oregonian

[ Tue, Feb 24th ]: The Jerusalem Post Blogs

[ Tue, Feb 24th ]: Los Angeles Times

[ Tue, Feb 24th ]: Newsweek

[ Tue, Feb 24th ]: WTOP News

[ Tue, Feb 24th ]: CNBC

[ Tue, Feb 24th ]: The Boston Globe

[ Tue, Feb 24th ]: KUTV

[ Tue, Feb 24th ]: syracuse.com

[ Tue, Feb 24th ]: Dallas Morning News

[ Tue, Feb 24th ]: Wales Online

[ Tue, Feb 24th ]: Daily Record

[ Tue, Feb 24th ]: The Mirror

[ Tue, Feb 24th ]: The New Zealand Herald

[ Tue, Feb 24th ]: Jerry

[ Tue, Feb 24th ]: Daily Express

[ Mon, Feb 23rd ]: AOL

[ Mon, Feb 23rd ]: Mediaite

[ Mon, Feb 23rd ]: ThePrint

[ Mon, Feb 23rd ]: HousingWire

[ Mon, Feb 23rd ]: Variety

[ Mon, Feb 23rd ]: Newsweek

[ Mon, Feb 23rd ]: moneycontrol.com

[ Mon, Feb 23rd ]: Penn Live

[ Mon, Feb 23rd ]: Fox Business

[ Mon, Feb 23rd ]: Daily Mail

[ Mon, Feb 23rd ]: Fortune

[ Mon, Feb 23rd ]: Daily Express

[ Mon, Feb 23rd ]: Sporting News

Mortgage Rates Fall to Lowest Point Since August 2023

HousingWire

HousingWireLocale: UNITED STATES

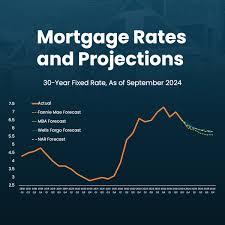

Monday, February 23rd, 2026 - After months of fluctuating amidst economic uncertainty, mortgage rates have offered a beacon of hope to potential homebuyers and existing homeowners alike. The average 30-year fixed-rate mortgage has fallen to 6.99%, marking the lowest point since August 2023, according to recent data from Freddie Mac. While still significantly elevated compared to the historically low rates seen in recent years, this decline is prompting analysts to cautiously suggest a potential shift in the housing market dynamic.

Just last year, the average 30-year fixed-rate mortgage hovered around a remarkably low 3.57%. The rapid ascent of rates since then has dramatically impacted affordability, sidelining many would-be buyers and dampening housing sales across the nation. However, the current dip, from 7.12% the previous week, signals a possible easing of the pressure.

Decoding the Spread: A Key Indicator

Beyond the headline rate, the shrinking gap - or 'spread' - between mortgage rates and U.S. Treasury yields is drawing significant attention from market observers. This spread represents the premium investors demand for the added risk of lending to homeowners compared to the perceived safety of government bonds. Historically, a narrowing spread has been a reliable precursor to improved market conditions and further declines in mortgage rates.

Logan Gerard, housing economist at Freddie Mac, explains, "The confluence of slowing interest rate hikes and moderating inflation data is the primary driver behind both the narrowing spread and the decrease in mortgage rates." This suggests that the Federal Reserve's tightening cycle may be nearing its end, providing some relief to the mortgage market. However, Gerard cautions that "affordability remains a key constraint," emphasizing that the benefits of lower rates are somewhat offset by persistent high home prices.

Affordability: The Lingering Challenge

Despite the positive trend in rates, the dream of homeownership remains out of reach for a substantial portion of the population. The twin forces of elevated home prices - a legacy of pandemic-era demand and limited inventory - and ongoing inflationary pressures continue to stretch household budgets. While the rate decline is welcome, it's crucial to remember that even a modest decrease doesn't fully counteract the impact of higher prices.

Data suggests that housing inventory remains tight in many markets, particularly for entry-level homes. This limited supply keeps prices elevated, preventing a significant improvement in affordability. Furthermore, the lingering effects of inflation on other essential household expenses - groceries, utilities, transportation - reduce the amount of disposable income available for housing costs.

Looking Ahead: What Will Drive Future Rates?

The future trajectory of mortgage rates hinges on several key factors. Foremost among these is the Federal Reserve's monetary policy. Analysts are closely monitoring upcoming economic data releases, particularly inflation reports and employment figures, for clues about the Fed's next move. A sustained slowdown in inflation would likely embolden the Fed to pause or even reverse its tightening policy, potentially leading to further rate declines.

Another crucial factor is the state of the U.S. economy. A weakening economy could prompt the Fed to lower rates to stimulate growth, while a robust economy could lead to continued inflationary pressures and potentially higher rates. The interplay between these forces will be complex and unpredictable.

Opportunity Knocks, But Caution is Advised

The current rate environment presents a potential opportunity for both homebuyers and those looking to refinance. Those who have been waiting for rates to fall may find the current levels more attractive. However, experts urge caution. It's essential to carefully assess your financial situation and consider your long-term goals before making any significant decisions.

Furthermore, it's vital to be prepared for potential fluctuations. While the current trend is encouraging, there is no guarantee that rates will continue to fall. Monitoring market developments and seeking advice from a qualified mortgage professional is highly recommended.

Finally, the rise of innovative mortgage products - including adjustable-rate mortgages (ARMs) and rate buydowns - offers alternative pathways to homeownership, but these options come with their own set of risks and benefits that must be thoroughly understood.

Read the Full HousingWire Article at:

https://www.housingwire.com/articles/mortgage-rates-under-6-spreads/

[ Sun, Feb 22nd ]: Fortune

[ Fri, Feb 20th ]: Fortune

[ Thu, Feb 19th ]: wjla

[ Fri, Feb 13th ]: Fox Business

[ Tue, Feb 10th ]: Fortune

[ Fri, Feb 06th ]: Fortune

[ Fri, Feb 06th ]: HousingWire

[ Fri, Feb 06th ]: Fortune

[ Thu, Feb 05th ]: WTOP News

[ Tue, Feb 03rd ]: Fortune

[ Mon, Feb 02nd ]: Fortune

[ Mon, Jan 12th ]: Fortune