[ Fri, Nov 07th 2025 ]: Newsweek

[ Fri, Nov 07th 2025 ]: Fortune

[ Fri, Nov 07th 2025 ]: BBC

[ Thu, Nov 06th 2025 ]: The Boston Globe

[ Thu, Nov 06th 2025 ]: WNYT NewsChannel 13

[ Thu, Nov 06th 2025 ]: WDIO

[ Thu, Nov 06th 2025 ]: The Courier-Journal

[ Thu, Nov 06th 2025 ]: Berkshire Eagle

[ Thu, Nov 06th 2025 ]: KY3

[ Thu, Nov 06th 2025 ]: WMUR

[ Thu, Nov 06th 2025 ]: Global News

[ Thu, Nov 06th 2025 ]: KDFW

[ Thu, Nov 06th 2025 ]: Toronto Star

[ Thu, Nov 06th 2025 ]: Action News Jax

[ Thu, Nov 06th 2025 ]: WABI-TV

[ Thu, Nov 06th 2025 ]: WSMV

[ Thu, Nov 06th 2025 ]: HousingWire

[ Thu, Nov 06th 2025 ]: USA Today

[ Thu, Nov 06th 2025 ]: Bloomberg L.P.

[ Thu, Nov 06th 2025 ]: KOB 4

[ Thu, Nov 06th 2025 ]: WSB-TV

[ Thu, Nov 06th 2025 ]: Fox News

[ Thu, Nov 06th 2025 ]: Sporting News

[ Thu, Nov 06th 2025 ]: tmz.com

[ Thu, Nov 06th 2025 ]: HoopsHype

[ Thu, Nov 06th 2025 ]: Newsweek

[ Thu, Nov 06th 2025 ]: Fortune

[ Thu, Nov 06th 2025 ]: BBC

[ Wed, Nov 05th 2025 ]: Hawaii News Now

[ Wed, Nov 05th 2025 ]: KUTV

[ Wed, Nov 05th 2025 ]: The Indianapolis Star

[ Wed, Nov 05th 2025 ]: KMBC Kansas City

[ Wed, Nov 05th 2025 ]: HoopsHype

[ Wed, Nov 05th 2025 ]: KHQ

[ Wed, Nov 05th 2025 ]: MarketWatch

[ Wed, Nov 05th 2025 ]: NerdWallet

[ Wed, Nov 05th 2025 ]: Milwaukee Journal Sentinel

[ Wed, Nov 05th 2025 ]: Fox News

[ Wed, Nov 05th 2025 ]: Fortune

[ Wed, Nov 05th 2025 ]: The Cincinnati Enquirer

[ Tue, Nov 04th 2025 ]: Investopedia

[ Tue, Nov 04th 2025 ]: HousingWire

[ Tue, Nov 04th 2025 ]: Newsweek

[ Tue, Nov 04th 2025 ]: Business Insider

[ Tue, Nov 04th 2025 ]: Detroit News

[ Tue, Nov 04th 2025 ]: USA Today

[ Tue, Nov 04th 2025 ]: Fortune

[ Tue, Nov 04th 2025 ]: BBC

Current mortgage rates report for Nov. 5, 2025: Rates tick up slightly | Fortune

Fortune

Fortune

Current Mortgage Rates – November 5 2025

As the United States enters the final quarter of 2025, mortgage rates remain a critical barometer for both prospective homeowners and seasoned refinancers. On November 5, the average rates reported across major benchmark lenders illustrate a market that has tightened in recent months, yet still reflects a degree of volatility driven by Federal Reserve policy, Treasury yields, and broader macro‑economic forces.

30‑Year Fixed‑Rate Mortgage

The 30‑year fixed‑rate, the most popular product for first‑time buyers and long‑term owners, is hovering at 6.12 %. This figure represents a modest decline of roughly 0.07 % from the prior month’s average of 6.19 %. While still above the 5.30 % average seen in early 2024, the rate remains in a range that many lenders regard as “moderate.” The reduction is attributed largely to a slight dip in the 10‑year Treasury yield, which fell from 4.28 % to 4.23 % over the past four weeks.

A comparison to the mortgage bankers’ association’s monthly “Median Rate” series shows that the 30‑year rate is 0.04 % higher than the median reported in the same period. The difference underscores that certain large lenders continue to offer rates on the lower end of the spectrum, while a broader cohort keeps rates closer to the 6.12 % average.

15‑Year Fixed‑Rate Mortgage

For borrowers who favor a shorter term and a higher monthly payment in exchange for lower overall interest costs, the 15‑year fixed‑rate is listed at 5.45 %. This rate is down 0.03 % from the previous month’s 5.48 %. The 15‑year rate mirrors the 30‑year trend, with the primary difference being the slightly tighter spread that generally characterizes the shorter‑term product.

The 15‑year’s relatively stable performance indicates that, while the market continues to react to Fed signals, investors are maintaining confidence in the long‑term U.S. debt market’s safety. According to Freddie Mac’s “Mortgage Rate Tracker,” the 15‑year median remains consistent with the broader industry average, suggesting that rate‑setting committees at major banks have largely converged on a similar risk appetite.

Adjustable‑Rate Mortgages (ARMs)

Adjustable‑rate mortgages provide an alternative for borrowers looking to lock in a lower initial rate with the possibility of future adjustments. On November 5, the 5/1 ARM was at 5.68 %, a slight uptick of 0.02 % from the prior month’s 5.66 %. Meanwhile, the 7/1 ARM settled at 5.81 %, unchanged from the previous report.

These rates reflect the benchmark 5‑year Treasury note, which sits at 3.75 %—just below the 3.85 % level that historically aligns with the 5/1 ARM. The 7/1 ARM’s marginal increase correlates with a modest rise in the 7‑year Treasury, indicating that investors are pricing in slightly higher risk for the longer adjustable period.

Drivers Behind the Numbers

Federal Reserve Policy

The Fed has been in a tightening cycle, raising its target range by a cumulative 1.75 % over the past 12 months. While the latest policy meeting signaled a pause in rate hikes, the 25‑basis‑point increase announced in August set a new baseline that is still reflected in mortgage pricing.Treasury Yields

Treasury yields are the primary benchmark for mortgage rates. A 10‑year yield of 4.23 % translates into a “spread” that lenders add to derive their quoted rates. When the Treasury market dips, as it has slightly in October, mortgage rates typically follow.Inflation and Economic Growth

Inflation, which has moderated from the 5.4 % peak in mid‑2024 to roughly 3.2 % in October, continues to weigh on rates. Lower inflation expectations reduce the Fed’s incentive to tighten further, thereby stabilizing rates. Simultaneously, robust economic growth—indicated by a 2.3 % GDP expansion in Q3 2025—supports a higher demand for credit, pushing rates up.Housing Market Conditions

The U.S. housing inventory remains tight, with home sales rising 3.5 % month‑over‑month as of November. High demand keeps sellers’ prices steady, thereby sustaining the need for mortgage financing. Refinancing activity, which accounted for 15 % of the market in October, has increased as homeowners seek to lock in the latest lower rates.

What This Means for Homebuyers and Refinancers

First‑Time Buyers: With a 30‑year fixed at 6.12 %, the monthly payment on a $300,000 loan is approximately $1,796, not including taxes, insurance, and HOA fees. While this is higher than last year’s $1,520 figure, the 6.12 % rate remains competitive relative to the 6.30 % average of early 2025.

Existing Homeowners: Refinancing could still be attractive if your current mortgage is 5‑year‑fixed or older. The spread between your rate and the current 30‑year average may offer savings of $80–$120 per month on a typical loan, depending on the remaining balance and loan term.

Investors: Those seeking fixed‑rate exposure can consider 15‑year fixed products to reduce interest expense, though the monthly payment will be higher. ARMs remain an option for those comfortable with payment variability, especially if they plan to sell or refinance before the adjustment period.

Outlook

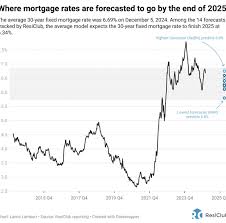

Industry analysts predict that mortgage rates will remain in the 6.00 %–6.30 % range for the remainder of 2025, barring unexpected Fed policy shifts or a sudden change in Treasury yields. The current pause in rate hikes suggests that the Fed may allow rates to settle, but inflationary pressures and global economic uncertainty mean that a sudden uptick cannot be ruled out.

Key Takeaways

- 30‑Year Fixed: 6.12 % (down 0.07 % month‑over‑month).

- 15‑Year Fixed: 5.45 % (down 0.03 %).

- 5/1 ARM: 5.68 %.

- 7/1 ARM: 5.81 %.

- Primary Drivers: Fed policy, Treasury yields, inflation, and housing demand.

- Actionable Advice: First‑time buyers should weigh the cost of higher payments against the benefits of homeownership; existing homeowners should compare refinancing costs to potential savings; investors can use ARMs or shorter fixed terms based on risk tolerance.

As the market continues to evolve, staying attuned to daily rate changes and Fed statements will remain essential for anyone navigating the mortgage landscape in late 2025.

Read the Full Fortune Article at:

https://fortune.com/article/current-mortgage-rates-11-05-2025/

[ Tue, Nov 04th 2025 ]: Fortune

[ Fri, Oct 24th 2025 ]: Fortune

[ Thu, Oct 23rd 2025 ]: Channel 3000

[ Tue, Oct 21st 2025 ]: Fortune

[ Fri, Oct 17th 2025 ]: Fortune

[ Wed, Oct 15th 2025 ]: NerdWallet

[ Mon, Oct 06th 2025 ]: fingerlakes1

[ Fri, Sep 12th 2025 ]: Local 12 WKRC Cincinnati

[ Thu, Sep 11th 2025 ]: Fortune

[ Tue, Sep 09th 2025 ]: WGME

[ Tue, Sep 09th 2025 ]: NerdWallet

[ Thu, Sep 04th 2025 ]: Fortune