[ Mon, Oct 27th 2025 ]: Cleveland.com

[ Mon, Oct 27th 2025 ]: HousingWire

[ Mon, Oct 27th 2025 ]: Journal Star

[ Mon, Oct 27th 2025 ]: BBC

[ Mon, Oct 27th 2025 ]: Fox 11 News

[ Sun, Oct 26th 2025 ]: World Socialist Web Site

[ Sun, Oct 26th 2025 ]: KOB 4

[ Sun, Oct 26th 2025 ]: WYFF

[ Sun, Oct 26th 2025 ]: Tennessean

[ Sun, Oct 26th 2025 ]: KSTP-TV

[ Sat, Oct 25th 2025 ]: MedPage Today

[ Sat, Oct 25th 2025 ]: Daily Press

[ Sat, Oct 25th 2025 ]: MLive

[ Sat, Oct 25th 2025 ]: People

[ Sat, Oct 25th 2025 ]: Arizona Daily Star

[ Sat, Oct 25th 2025 ]: Channel 3000

[ Sat, Oct 25th 2025 ]: BBC

[ Sat, Oct 25th 2025 ]: The Motley Fool

[ Fri, Oct 24th 2025 ]: Newsweek

[ Fri, Oct 24th 2025 ]: Eagle-Tribune

[ Fri, Oct 24th 2025 ]: Associated Press

[ Fri, Oct 24th 2025 ]: RTE Online

[ Fri, Oct 24th 2025 ]: The Outerhaven

[ Fri, Oct 24th 2025 ]: syracuse.com

[ Fri, Oct 24th 2025 ]: Fortune

[ Fri, Oct 24th 2025 ]: BBC

[ Fri, Oct 24th 2025 ]: HousingWire

[ Fri, Oct 24th 2025 ]: moneycontrol.com

[ Thu, Oct 23rd 2025 ]: The Raw Story

[ Thu, Oct 23rd 2025 ]: USA Today

[ Thu, Oct 23rd 2025 ]: Chattanooga Times Free Press

[ Thu, Oct 23rd 2025 ]: Investopedia

[ Thu, Oct 23rd 2025 ]: Detroit News

[ Thu, Oct 23rd 2025 ]: WDIO

[ Thu, Oct 23rd 2025 ]: Oregonian

[ Thu, Oct 23rd 2025 ]: Channel 3000

[ Thu, Oct 23rd 2025 ]: HousingWire

[ Thu, Oct 23rd 2025 ]: Associated Press

[ Thu, Oct 23rd 2025 ]: Bravo

[ Thu, Oct 23rd 2025 ]: Seeking Alpha

[ Thu, Oct 23rd 2025 ]: People

[ Thu, Oct 23rd 2025 ]: MarketWatch

[ Thu, Oct 23rd 2025 ]: Washington Examiner

[ Thu, Oct 23rd 2025 ]: BBC

[ Thu, Oct 23rd 2025 ]: The Courier-Journal

[ Thu, Oct 23rd 2025 ]: FXStreet

[ Thu, Oct 23rd 2025 ]: HELLO! Magazine

[ Thu, Oct 23rd 2025 ]: Fortune

This one number explains the growing gulf between people who can afford to buy a house today -- and those who can't

MarketWatch

MarketWatch

The Rising Price‑to‑Income Ratio: A Sharp Lens on America’s Housing Divide

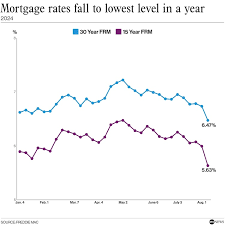

The housing market’s growing divide between those who can purchase a home and those who cannot can be distilled into a single metric: the median price‑to‑income ratio. In recent years this ratio has climbed from roughly 4.6 in the late 2000s to around 5.7 today, a jump that underscores how quickly home prices are outpacing wage growth and erodes the notion that a house is a universal milestone.

What the Number Means

The price‑to‑income ratio is calculated by dividing the median home price by the median household income. If the ratio is 4.5, it means a household would need roughly 4.5 times its annual income to afford a median‑priced home—assuming no other debts, a typical 20‑percent down payment, and current mortgage rates. A ratio above 5 signals that the average household would need more than five times its income to comfortably buy a home, a level that strains many families.

Data from the U.S. Census Bureau and the S&P/Case‑Shiller Home Price Index show that median U.S. home prices topped $400,000 in 2023, while median household income hovered around $70,000. That places the ratio at approximately 5.7, a figure that has remained above the long‑term average of about 4.5 for the last decade.

Historical Context and the Pandemic Surge

The ratio was at its lowest point in the early 2010s, after the 2008 financial crisis, when falling home prices and rising unemployment compressed the metric to below 4. The subsequent decade of low mortgage rates and steady income growth pulled the ratio back up, but it never fully recovered to pre‑2008 levels.

The COVID‑19 pandemic added a new layer of complexity. For a brief period in 2020, as mortgage rates hit historic lows, the ratio dipped slightly. However, the rapid rebound of home prices—surging 25‑30 percent in 2021—outpaced the modest rise in median incomes, pushing the ratio back into the high 5s by late 2022.

Supply Constraints and Policy Factors

Housing supply is a key driver behind the rising ratio. In many U.S. metropolitan areas, zoning laws and local land‑use regulations limit the density of new housing units, keeping construction costs high. Meanwhile, the supply of affordable housing units—those priced below 60 percent of the area median income—has been shrinking. A 2022 Freddie Mac report found that the stock of affordable homes declined by 4 percent over a five‑year period, further tightening the market.

Policy decisions at the federal, state, and local levels also influence affordability. The 2021 American Rescue Plan Act temporarily capped mortgage rates at 2.5 percent for new homebuyers, but the effect was short‑lived. Conversely, increasing mortgage‑originating fees and higher down‑payment requirements have made it harder for first‑time buyers to enter the market.

Who’s Most Affected

The price‑to‑income ratio paints a stark picture of generational inequality. Millennials, who entered the workforce during the Great Recession, are still battling for homeownership. Their median household income is roughly $75,000, but the median price of their local market can be well above $400,000, leaving many to remain renters. Even for the traditional “middle class”—households earning $100,000 or more—the ratio suggests that a typical home costs more than five times an average salary, a cost that strains budgets and limits saving potential.

High‑income earners, meanwhile, can afford multiple homes, and their wealth can grow through appreciation, while low‑income households face the dual challenge of paying rent and living with high interest costs on credit cards and auto loans. The widening gulf contributes to the broader wealth gap: homeowners build equity, renters do not.

Potential Paths Forward

A handful of strategies could help bring the ratio back toward a more affordable range:

Zoning Reform – Encouraging higher‑density housing, reducing parking mandates, and streamlining permit processes can lower construction costs.

Incentivizing Affordable Housing – Tax credits and public‑private partnerships can increase the supply of units priced below 60 percent of the area median income.

Adjusting Mortgage Policies – Expanding access to low‑down‑payment loans and stabilizing mortgage‑originating fees can help first‑time buyers.

Broadening Income Growth – Strengthening labor market policies to boost wages, particularly in the construction and skilled trades, can help balance the ratio.

Conclusion

The median price‑to‑income ratio is more than a statistic; it’s a barometer of the health of the American housing market and the equitable distribution of wealth. As median home prices continue to rise faster than wages, the gulf between buyers and renters widens. Addressing this divide will require coordinated policy changes that increase supply, protect affordability, and ensure that the dream of homeownership remains attainable for all.

Read the Full MarketWatch Article at:

[ https://www.marketwatch.com/story/this-one-number-explains-the-growing-gulf-between-people-who-can-afford-to-buy-a-house-today-and-those-who-cant-2fd6dcd7 ]

[ Mon, Oct 13th 2025 ]: Newsweek

[ Sun, Sep 21st 2025 ]: KTBS

[ Wed, Sep 17th 2025 ]: HousingWire

[ Wed, Sep 17th 2025 ]: Las Vegas Review-Journal

[ Sun, Sep 14th 2025 ]: WTOP News

[ Thu, Sep 11th 2025 ]: KIRO-TV

[ Wed, Sep 10th 2025 ]: HousingWire

[ Tue, Sep 09th 2025 ]: WSB-TV

[ Tue, Sep 09th 2025 ]: rnz

[ Tue, Sep 09th 2025 ]: WCVB Channel 5 Boston

[ Mon, Sep 08th 2025 ]: The Baltimore Sun

[ Mon, Sep 08th 2025 ]: Channel 3000