[ Mon, Oct 27th 2025 ]: Valley News Live

[ Mon, Oct 27th 2025 ]: Fortune

[ Mon, Oct 27th 2025 ]: ESPN

[ Mon, Oct 27th 2025 ]: KIRO-TV

[ Mon, Oct 27th 2025 ]: News 8000

[ Mon, Oct 27th 2025 ]: YourTango

[ Mon, Oct 27th 2025 ]: InStyle

[ Mon, Oct 27th 2025 ]: Cleveland.com

[ Mon, Oct 27th 2025 ]: HousingWire

[ Mon, Oct 27th 2025 ]: Journal Star

[ Mon, Oct 27th 2025 ]: BBC

[ Mon, Oct 27th 2025 ]: Fox 11 News

[ Sun, Oct 26th 2025 ]: World Socialist Web Site

[ Sun, Oct 26th 2025 ]: KOB 4

[ Sun, Oct 26th 2025 ]: WYFF

[ Sun, Oct 26th 2025 ]: Tennessean

[ Sun, Oct 26th 2025 ]: KSTP-TV

[ Sat, Oct 25th 2025 ]: MedPage Today

[ Sat, Oct 25th 2025 ]: Daily Press

[ Sat, Oct 25th 2025 ]: MLive

[ Sat, Oct 25th 2025 ]: People

[ Sat, Oct 25th 2025 ]: Arizona Daily Star

[ Sat, Oct 25th 2025 ]: Channel 3000

[ Sat, Oct 25th 2025 ]: BBC

[ Sat, Oct 25th 2025 ]: The Motley Fool

[ Fri, Oct 24th 2025 ]: Newsweek

[ Fri, Oct 24th 2025 ]: Eagle-Tribune

[ Fri, Oct 24th 2025 ]: Associated Press

[ Fri, Oct 24th 2025 ]: RTE Online

[ Fri, Oct 24th 2025 ]: The Outerhaven

[ Fri, Oct 24th 2025 ]: syracuse.com

[ Fri, Oct 24th 2025 ]: Fortune

[ Fri, Oct 24th 2025 ]: BBC

[ Fri, Oct 24th 2025 ]: HousingWire

[ Fri, Oct 24th 2025 ]: moneycontrol.com

[ Thu, Oct 23rd 2025 ]: The Raw Story

[ Thu, Oct 23rd 2025 ]: USA Today

[ Thu, Oct 23rd 2025 ]: Investopedia

[ Thu, Oct 23rd 2025 ]: Detroit News

[ Thu, Oct 23rd 2025 ]: Oregonian

[ Thu, Oct 23rd 2025 ]: HousingWire

[ Thu, Oct 23rd 2025 ]: Associated Press

[ Thu, Oct 23rd 2025 ]: Seeking Alpha

[ Thu, Oct 23rd 2025 ]: BBC

[ Thu, Oct 23rd 2025 ]: The Courier-Journal

[ Thu, Oct 23rd 2025 ]: FXStreet

[ Thu, Oct 23rd 2025 ]: HELLO! Magazine

[ Thu, Oct 23rd 2025 ]: Fortune

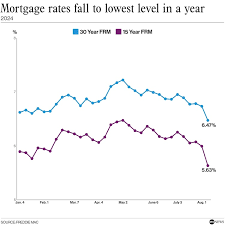

Average mortgage rate drops to lowest level in more than a year

Oregonian

Oregonian

Average U.S. Mortgage Rates Hit a Five‑Month Low, Signaling a Possible Buying Window

The latest data from Freddie Mac reveals that the national average for 30‑year fixed‑rate mortgages fell to 7.23 %, a new low not seen since March 2024. The dip follows a modest decline in Treasury yields and an easing of expectations around the Federal Reserve’s future policy stance, and it has prompted a wave of optimism across the housing market, especially in high‑cost states such as Oregon.

Key Figures and the Broader Context

Freddie Mac’s weekly mortgage rate report shows a steady decline in the average 30‑year fixed rate, which has eased from 7.30 % in the previous week to 7.23 %. The 15‑year fixed rate also slipped to 7.00 % from 7.08 %, while the average 10‑year adjustable‑rate mortgage (ARM) fell to 7.70 % from 7.78 %. These numbers place the market on the cusp of a historic low, and analysts are interpreting the trend as a sign that borrowing costs are becoming more accessible for the average homebuyer.

The article references the Federal Reserve’s recent policy meeting, where the central bank signaled that it will likely hold the federal funds target rate near the 5.25–5.50 % range for an extended period. While the Fed remains committed to curbing inflation, the market has begun to absorb expectations of a slower rate of tightening, which has helped to push mortgage rates downward.

Freddie Mac’s data also shows that U.S. Treasury yields, a major driver of mortgage rates, have been trending lower. The 10‑year Treasury yield fell to 4.12 % in the most recent week, down from 4.20 %. This decline in yield, coupled with the Fed’s dovish stance, has created a more favorable environment for mortgage lenders and their borrowers alike.

Impact on Home Buying and Regional Variations

The fall in mortgage rates is expected to have a measurable impact on the housing market. According to the article, homebuyers in Oregon have reported a renewed sense of confidence, noting that the reduced rates translate into lower monthly payments and an expanded range of affordable homes. For a typical $450,000 home, a 30‑year fixed mortgage at 7.23 % would produce a monthly payment of approximately $3,000, whereas a 7.00 % rate would lower the payment to about $2,900—a difference of roughly $100 a month that can be a decisive factor for many families.

While the national average is the headline figure, the article also highlights that regional variations persist. In the Pacific Northwest, for instance, rates have slipped to 7.15 % for 30‑year fixed mortgages, slightly lower than the national average. This regional dip is partially attributed to a higher concentration of adjustable‑rate products in that market, which tend to lag behind fixed‑rate pricing. The article links to a separate market snapshot for Oregon, which shows that home prices in the Portland metro area have moderated by about 2.5 % over the past year, easing affordability concerns to a degree.

Expert Commentary and Forward Outlook

Real‑estate analysts in the article caution that while rates have reached a historic low, they may still rise in the coming months if inflationary pressures prove persistent. A quoted expert, a senior economist at a regional mortgage brokerage, warned that the Federal Reserve could consider a rate hike in the third quarter of 2025 if the inflation gauge fails to reach its 2 % target. In contrast, other market watchers are optimistic that the easing of Treasury yields will outpace any Fed tightening, keeping mortgage rates comfortably low for the next 12 to 18 months.

The article also points to a new Freddie Mac mortgage affordability calculator, a tool that lets consumers input their income, credit score, and desired down payment to estimate the maximum home price they can afford at current rates. The tool, which is linked within the article, has been adopted by many prospective buyers looking to quantify their buying power in a shifting market.

Broader Implications for the Housing Market

Historically, lower mortgage rates spur home sales by making financing more attractive. The article cites recent data indicating that U.S. home sales rose by 3.2 % in September, a modest but noteworthy uptick that analysts attribute partly to falling rates. The rise in sales is being seen as a positive sign for the broader economy, as increased homeownership can stimulate local spending on furnishings, renovations, and related services.

In Oregon, the housing market has been grappling with a supply‑demand imbalance for several years. The article references a local study that found inventory levels remain at 12‑month lows, meaning that even modest rate reductions may not immediately unlock the market’s potential. Nevertheless, the article suggests that a sustained period of low rates could help slow the rate of price appreciation, making homes more attainable for first‑time buyers and improving overall affordability.

Conclusion

The drop in average mortgage rates to a five‑month low is a significant development for the U.S. housing market, especially in high‑cost states like Oregon. While the decline brings relief to many prospective homebuyers, it also underscores the importance of remaining vigilant about the broader economic signals that could alter the trajectory of rates in the near future. As the Federal Reserve keeps its eye on inflation, mortgage rates may oscillate, but the current environment offers a window of opportunity for those looking to enter or expand their position in the real‑estate market.

Read the Full Oregonian Article at:

[ https://www.oregonlive.com/realestate/2025/10/average-mortgage-rate-drops-to-lowest-level-in-more-than-a-year.html ]

[ Wed, Oct 22nd 2025 ]: Local 12 WKRC Cincinnati

[ Tue, Oct 21st 2025 ]: Fortune

[ Fri, Oct 17th 2025 ]: Fortune

[ Fri, Oct 10th 2025 ]: reuters.com

[ Mon, Oct 06th 2025 ]: fingerlakes1

[ Tue, Sep 30th 2025 ]: Fortune

[ Mon, Sep 29th 2025 ]: NerdWallet

[ Tue, Sep 23rd 2025 ]: HousingWire

[ Wed, Sep 10th 2025 ]: HousingWire

[ Thu, Sep 04th 2025 ]: Fortune

[ Fri, Aug 08th 2025 ]: Fortune

[ Mon, Aug 04th 2025 ]: CNET