[ Wed, Feb 25th ]: wjla

[ Wed, Feb 25th ]: Fox 11 News

[ Wed, Feb 25th ]: Seeking Alpha

[ Wed, Feb 25th ]: MarketWatch

[ Wed, Feb 25th ]: The Independent

[ Wed, Feb 25th ]: Daily Camera

[ Wed, Feb 25th ]: FOX 5 Atlanta

[ Wed, Feb 25th ]: WGME

[ Wed, Feb 25th ]: Fortune

[ Wed, Feb 25th ]: Daily Mail

[ Wed, Feb 25th ]: Cleveland.com

[ Wed, Feb 25th ]: Birmingham Mail

[ Wed, Feb 25th ]: WISH-TV

[ Wed, Feb 25th ]: 7NEWS

[ Wed, Feb 25th ]: The Center Square

[ Wed, Feb 25th ]: Billboard

[ Wed, Feb 25th ]: CBS News

[ Wed, Feb 25th ]: Daily Record

[ Wed, Feb 25th ]: Local 12 WKRC Cincinnati

[ Wed, Feb 25th ]: WSB Radio

[ Wed, Feb 25th ]: KGNS-TV

[ Wed, Feb 25th ]: WTOP News

[ Wed, Feb 25th ]: The West Australian

[ Wed, Feb 25th ]: NBC Los Angeles

[ Wed, Feb 25th ]: The Clarion-Ledger

[ Tue, Feb 24th ]: CNN

[ Tue, Feb 24th ]: Daily Mail

[ Tue, Feb 24th ]: Euronews

[ Tue, Feb 24th ]: BBC

[ Tue, Feb 24th ]: Forbes

[ Tue, Feb 24th ]: NBC News

[ Tue, Feb 24th ]: The Courier-Journal

[ Tue, Feb 24th ]: People

[ Tue, Feb 24th ]: 7NEWS

[ Tue, Feb 24th ]: Fortune

[ Tue, Feb 24th ]: Detroit Free Press

[ Tue, Feb 24th ]: Irish Examiner

[ Tue, Feb 24th ]: Fox News

[ Tue, Feb 24th ]: HousingWire

[ Tue, Feb 24th ]: Variety

[ Tue, Feb 24th ]: Sporting News

[ Tue, Feb 24th ]: Oregonian

[ Tue, Feb 24th ]: Los Angeles Times

[ Tue, Feb 24th ]: Newsweek

[ Tue, Feb 24th ]: WTOP News

[ Tue, Feb 24th ]: The Boston Globe

[ Tue, Feb 24th ]: Daily Record

[ Tue, Feb 24th ]: The New Zealand Herald

Mortgage Rates Plummet, Sparking Housing Market Optimism

Fortune

FortuneLocale: UNITED STATES

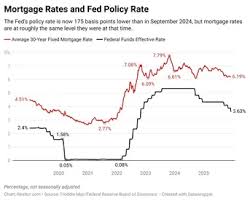

Tuesday, February 24th, 2026 - After a prolonged period of high interest rates that choked housing affordability, prospective homebuyers are finally seeing a glimmer of hope. Mortgage rates have experienced a substantial drop, falling to their lowest levels since late 2023, sparking optimism for a reinvigorated housing market this spring. As of today, the average 30-year fixed mortgage rate hovers around 5.8%, a welcome decrease from the peaks seen throughout 2024, which at times exceeded 7.5%.

This decline isn't merely a statistical blip; it represents a significant shift in the economic landscape and has the potential to reshape the dynamics of the real estate sector. The ripple effects are already being felt, and experts predict a surge in activity as buyers, previously sidelined by high costs, re-enter the market.

The Anatomy of a Rate Drop: Beyond Inflation

The primary driver behind this downward trend is a cooling of inflationary pressures. While inflation hasn't vanished entirely, recent economic data demonstrates a consistent deceleration, convincing investors that the Federal Reserve may soon pivot from its aggressive tightening policy. This expectation of a less hawkish stance from the Fed is the most influential factor.

However, the story is more nuanced than just inflation. The 10-year Treasury yield, a key benchmark for mortgage rates, has also fallen, reflecting broader investor confidence and expectations of slower economic growth. This interrelation highlights the complex interplay between global financial markets and domestic housing affordability. The Fed's increasingly explicit signaling - what analysts term a "dovish shift" - has been critical. Comments from Federal Reserve officials suggesting a potential pause in rate hikes, and even hinting at possible rate cuts later in the year, have directly translated into lower mortgage rates.

A Market on the Cusp of Change: Buyers, Sellers, and Inventory

The impact of these lower rates is expected to be multifaceted. For potential homebuyers, the most immediate benefit is increased affordability. A decrease of nearly two percentage points in mortgage rates translates to hundreds of dollars in monthly savings, opening up homeownership to a wider segment of the population. This increased purchasing power is expected to drive demand, potentially alleviating some of the pent-up frustration experienced by those who've been waiting for more favorable conditions.

Sellers also stand to benefit. Lower rates will attract more buyers, creating a more competitive environment and potentially shortening the time properties remain on the market. While price increases aren't guaranteed, a surge in demand coupled with limited inventory could certainly push prices upward, particularly in desirable locations. However, the crucial variable remains inventory. If the supply of homes doesn't increase to meet the rising demand, the gains in affordability could be offset by renewed price competition.

Currently, housing inventory remains constrained in many markets, a lingering effect of underbuilding during the pandemic and subsequent supply chain disruptions. The extent to which this inventory shortage limits the impact of lower rates will be a key determinant of the market's trajectory.

Navigating the Uncertainty: What Lies Ahead?

Despite the positive trend, experts caution against complacency. Mortgage rates are notoriously volatile and sensitive to economic news. Unexpected inflation spikes, geopolitical events, or a shift in the Federal Reserve's outlook could quickly reverse the current gains. The economic calendar is littered with potential disruptors.

Looking ahead, potential homebuyers and sellers should remain vigilant and closely monitor economic indicators. Key data releases, including inflation reports, employment figures, and Federal Reserve announcements, will provide valuable insights into the direction of interest rates. Consulting with a qualified financial advisor and mortgage professional is crucial for making informed decisions tailored to individual circumstances.

The housing market is entering a period of transition, and while the current conditions are undeniably more favorable than they have been for quite some time, prudent planning and informed decision-making will be paramount for success. The spring housing market promises to be dynamic, but also requires careful consideration of the underlying economic forces at play. A return to the frenzied bidding wars of 2021-2022 is unlikely, but a healthy and competitive market is certainly within reach.

Read the Full Fortune Article at:

https://fortune.com/article/current-mortgage-rates-01-15-2026/

[ Mon, Feb 23rd ]: HousingWire

[ Mon, Feb 23rd ]: Fortune

[ Sun, Feb 22nd ]: Fortune

[ Fri, Feb 20th ]: Fortune

[ Thu, Feb 19th ]: wjla

[ Tue, Feb 10th ]: Fortune

[ Fri, Feb 06th ]: Fortune

[ Fri, Feb 06th ]: Fortune

[ Tue, Feb 03rd ]: Fortune

[ Mon, Feb 02nd ]: WSFA

[ Mon, Feb 02nd ]: Fortune

[ Fri, Nov 21st 2025 ]: HousingWire