by: socastsrm.com

China's home prices to fall less than previously expected, but market still weak: Reuters poll

by: The News-Herald

Average rate on a 30-year mortgage drops to 6.5%, lowest level since last October

by: Fortune

by: People

")

by: fingerlakes1

by: The Irish News

by: NY Post

Wild video shows entire house with cat inside floating away in Texas flooding, smashing into bridge

by: Global News

by: Seattle Times

White House's review of Smithsonian content could reach into classrooms nationwide

China's home prices to fall less than previously expected, but market still weak: Reuters poll

socastsrm.com

socastsrm.com

China’s Housing Market Shows Resilience: Prices Expected to Dip Less Than Anticipated, Yet the Sector Remains Strained

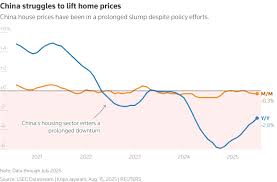

In a recent Reuters poll circulated among economists and market analysts, the consensus was that home prices in China will still decline over the next 12 months, but the fall will be more modest than earlier forecasts suggested. While the real‑estate sector remains the second‑largest pillar of the Chinese economy, the latest data indicate that the market is still grappling with a range of headwinds that threaten to stifle growth.

A Softer Slide in Prices

The poll, which gathered responses from 17 analysts across Asia and the United States, found that 62 % of respondents expect a price drop of between 1 % and 3 % over the next year, while 28 % foresee a decline of more than 3 %. By contrast, a survey conducted in June had projected a sharper fall, with 45 % of respondents predicting a 4 % or greater decrease. The adjustment reflects the market’s gradual adaptation to a set of policy changes and a more nuanced understanding of regional variations.

The average forecast for the National Housing Price Index (NHPI)—the key metric used to gauge nationwide price trends—now stands at a 0.6 % decline for the period from September 2024 to August 2025. This represents a 0.9‑percentage‑point lift from the June estimate of a −1.5 % drop. The latest projections are in line with the most recent data releases from the National Bureau of Statistics, which showed a 0.2 % month‑on‑month fall in the NHPI for August, compared with a 0.6 % drop in July.

Regional Disparities: Where Prices Are Holding

The poll also revealed a growing sense of geographic differentiation in price movements. While tier‑1 cities such as Shanghai and Beijing are still expected to experience modest declines—around 2 %—many tier‑2 and tier‑3 cities could see virtually flat or even modestly positive trends. The strongest resilience appears to be in the eastern coastal provinces of Jiangsu and Zhejiang, where the economy remains buoyant and demand for new housing has outpaced supply constraints.

In contrast, southern and western provinces, where the property market has been historically more speculative, continue to exhibit steeper declines. Analysts attribute this to a combination of over‑construction, rising inventory levels, and a cautious consumer sentiment that has been dampened by stricter mortgage lending guidelines.

Policy Moves: Cooling Measures and Market Stability

The Chinese government has implemented a range of measures in the past 18 months aimed at preventing a speculative bubble while avoiding a sharp contraction in the housing market. Key among these is the "Three Red Lines" policy, which sets thresholds for property‑development companies on debt levels relative to their assets, equity, and cash flow. While the policy has curbed excessive borrowing, it has also forced developers to reduce output, leading to a temporary supply slowdown.

Additionally, local governments have tightened the issuance of construction permits and increased the supply of land for sale in key urban centres, in an attempt to temper price inflation. The State Administration of Market Regulation has also introduced stricter verification processes for home purchases, making it harder for high‑net‑worth buyers to buy multiple properties.

The Ministry of Housing and Urban Development has issued a statement encouraging “balanced growth” and has pledged to support low‑income families through subsidies and tax incentives. Meanwhile, the People’s Bank of China has maintained its policy stance at a relatively low rate, but signalled that it may keep the 5‑year loan prime rate steady at 4.65 % for the near term.

Consumer Sentiment and Mortgage Conditions

Despite the moderating effect of policy, consumers remain wary. Credit‑rating agencies have flagged that the average mortgage debt-to-income ratio for first‑time homebuyers has risen by 1.5 % over the past year, indicating that borrowers are taking on more debt to secure property. The bank‑approved loan amount for new mortgages has also narrowed slightly, reflecting tighter underwriting standards.

Moreover, the “home‑ownership” culture in China—where owning property is seen as a prerequisite for social stability—continues to pressure demand, especially among younger demographics who are increasingly looking for more affordable housing options. Developers have responded by offering lower down‑payment schemes, but these have not fully offset the higher financing costs.

Economic Implications

China’s real‑estate sector accounts for roughly 28 % of national GDP, and its contraction has ripple effects on construction, raw‑material suppliers, and the overall financial system. A sharper price fall could trigger a wave of defaults among smaller developers, potentially jeopardising the financial stability of banks that hold large amounts of real‑estate‑related assets.

On the other hand, a moderate price decline—particularly in tier‑2 and tier‑3 cities—could help balance the market by re‑establishing a more sustainable demand‑supply equilibrium. Analysts note that a steady, moderate price decline may be preferable to a sharp drop that could trigger a chain reaction of defaults and financial distress.

Looking Ahead

The next key data points that will shape expectations include:

- The National Bureau of Statistics’ monthly housing‑price release for September 2025.

- The Ministry of Housing and Urban Development’s policy briefings regarding potential adjustments to land‑supply and loan‑terms.

- The China Banking Regulatory Commission’s review of mortgage‑lending practices across major banks.

As China continues to navigate the delicate balance between cooling speculative behaviour and sustaining growth in a critical economic sector, the real‑estate market will remain a bellwether for broader economic conditions. The recent shift in poll sentiment suggests that while the market still faces challenges, the risks may not be as acute as previously feared. Nevertheless, vigilance from policymakers, developers, and investors alike will be essential to prevent a systemic slowdown in the sector that could reverberate throughout the Chinese economy.

Sources: Reuters, National Bureau of Statistics, State Administration of Market Regulation, Ministry of Housing and Urban Development, China Banking Regulatory Commission.

Read the Full socastsrm.com Article at:

https://d2449.cms.socastsrm.com/2025/09/03/chinas-home-prices-to-fall-less-than-previously-expected-but-market-still-weak-reuters-poll/

on: Wed, Sep 03rd 2025

by: Newsweek

on: Sun, Aug 17th 2025

by: Business Insider

on: Sat, Aug 23rd 2025

by: Fortune

on: Tue, Aug 26th 2025

by: rnz

on: Tue, Aug 26th 2025

by: HousingWire

Home prices are still rising, but June numbers mark 'a decisive shift' in the housing market

on: Tue, Aug 26th 2025

by: HousingWire

on: Fri, Aug 08th 2025

by: Realtor.com

on: Fri, Aug 08th 2025

by: HousingWire

on: Wed, Jul 30th 2025

by: wjla

How Federal Reserve Interest Rates Impact the U.S. Housing Market

on: Tue, Sep 02nd 2025

by: rnz

on: Thu, Aug 28th 2025

by: Newsweek

Housing market hits troubling milestone for first time in nearly 20 years