[ Mon, Feb 23rd ]: Fox Business

[ Mon, Feb 23rd ]: Daily Mail

[ Mon, Feb 23rd ]: Fortune

[ Mon, Feb 23rd ]: Time Out

[ Mon, Feb 23rd ]: Daily Express

[ Mon, Feb 23rd ]: Sporting News

[ Sun, Feb 22nd ]: Carscoops

[ Sun, Feb 22nd ]: WCPO Cincinnati

[ Sun, Feb 22nd ]: Cleveland.com

[ Sun, Feb 22nd ]: krtv

[ Sun, Feb 22nd ]: London Evening Standard

[ Sun, Feb 22nd ]: syracuse.com

[ Sun, Feb 22nd ]: Patch

[ Sun, Feb 22nd ]: al.com

[ Sun, Feb 22nd ]: New York Post

[ Sun, Feb 22nd ]: Fox News

[ Sun, Feb 22nd ]: WJCL

[ Sun, Feb 22nd ]: The Mirror

[ Sun, Feb 22nd ]: fox13now

[ Sun, Feb 22nd ]: HELLO! Magazine

[ Sun, Feb 22nd ]: The Boston Globe

[ Sun, Feb 22nd ]: Post and Courier

[ Sun, Feb 22nd ]: WSB Radio

[ Sun, Feb 22nd ]: Townhall

[ Sun, Feb 22nd ]: Variety

[ Sun, Feb 22nd ]: Fortune

[ Sun, Feb 22nd ]: Popular Science

[ Sun, Feb 22nd ]: Local 12 WKRC Cincinnati

[ Sun, Feb 22nd ]: WSB-TV

[ Sun, Feb 22nd ]: WLWT

[ Sun, Feb 22nd ]: People

[ Sun, Feb 22nd ]: KIRO

[ Sun, Feb 22nd ]: BBC

[ Sun, Feb 22nd ]: IBTimes UK

[ Sun, Feb 22nd ]: Detroit Free Press

[ Sun, Feb 22nd ]: The Hill

[ Sun, Feb 22nd ]: Newsweek

[ Sun, Feb 22nd ]: WYFF

[ Sun, Feb 22nd ]: Seeking Alpha

[ Sun, Feb 22nd ]: MassLive

[ Sun, Feb 22nd ]: Sporting News

[ Sun, Feb 22nd ]: Metro

[ Sun, Feb 22nd ]: Daily Express

[ Sun, Feb 22nd ]: Toronto Star

[ Sun, Feb 22nd ]: Daily Mail

[ Sun, Feb 22nd ]: The New Indian Express

[ Sun, Feb 22nd ]: Parade

[ Sun, Feb 22nd ]: wtvr

Mortgage Rates Plunge to Lowest Levels Since 2020

Fortune

FortuneLocale: UNITED STATES

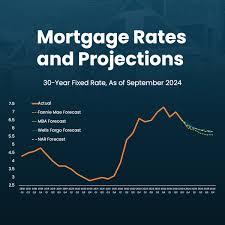

Sunday, February 22nd, 2026 - The housing market is experiencing a seismic shift as mortgage rates have plummeted to their lowest levels since early 2020. As of January 16th, 2026, the average 30-year fixed mortgage rate stands at a remarkably low 3.5%, igniting hope for prospective homebuyers and presenting attractive refinancing options for current homeowners. This article delves into the factors driving this dramatic decline, its implications for the future of the housing market, and what individuals can expect in the coming months.

The Tide Turns: Why Rates Are Falling

The primary catalyst behind this downward trend is the sustained moderation of inflation. Following a period of significant price increases across various sectors, inflationary pressures have begun to ease. This cooling effect has relieved some of the burden on the Federal Reserve, reducing the need to maintain aggressively high interest rates. The Federal Reserve has explicitly signaled its intention to implement interest rate cuts in the near future, a move that is further accelerating the decline in mortgage rates.

Odeta Kushi, Deputy Chief Economist at First American Financial, explains, "The data released this week unequivocally showed inflation continues to cool. This has naturally led to both speculation and anticipation of Federal Reserve rate cuts, which has directly helped push mortgage rates lower." The market's response to these signals has been swift and decisive, translating directly into lower borrowing costs for potential homebuyers.

A Boon for Buyers: Increased Affordability and Purchasing Power

Lower mortgage rates dramatically improve housing affordability. A 3.5% rate represents a substantial decrease compared to the highs experienced in recent years. This translates into lower monthly payments for borrowers over the lifetime of their loans, unlocking significant savings. Furthermore, lower rates effectively increase purchasing power, allowing buyers to qualify for larger loan amounts and, consequently, consider more expensive properties. This is particularly beneficial for first-time homebuyers who may have been priced out of the market previously.

Matthew Gardner, Chief Economist at Zillow, notes, "The drop in rates has been a very welcome change for buyers who have been effectively sidelined by high rates for the past couple of years." The impact is palpable, with increased foot traffic reported at open houses and a noticeable uptick in mortgage applications.

Refinancing Wave: Opportunities for Existing Homeowners

The benefits aren't limited to prospective buyers. Existing homeowners with adjustable-rate mortgages (ARMs) or those locked into higher interest rates on their fixed-rate loans are also presented with compelling refinancing opportunities. Securing a lower rate can significantly reduce monthly mortgage payments and potentially save tens of thousands of dollars over the life of the loan. This is particularly attractive for homeowners who took out mortgages when rates were considerably higher.

However, it's important to carefully evaluate the costs associated with refinancing, such as origination fees and appraisal costs, to ensure that the savings outweigh these expenses. A simple calculation of the break-even point--the time it takes to recoup these costs through lower monthly payments--can help homeowners make an informed decision.

Looking Ahead: Navigating Market Volatility

While the recent decline in mortgage rates is undoubtedly positive, experts urge caution and anticipate potential fluctuations. Several factors will continue to influence the trajectory of rates, including ongoing economic data releases, future inflation reports, and, crucially, the Federal Reserve's policy decisions.

Kushi cautions, "Mortgage rates are likely to remain relatively low in the near term, but volatility is still a very real possibility. It's essential to keep a close watch on the economic data and be prepared for potential shifts in the market." Geopolitical events and unexpected economic shocks could also contribute to market volatility.

The housing market is complex and influenced by a multitude of variables. While lower rates are a positive development, prospective buyers and homeowners should conduct thorough research, consult with financial advisors, and carefully assess their individual circumstances before making any significant financial decisions. The current environment presents opportunities, but informed decision-making remains paramount.

Disclaimer: Mortgage rates are subject to constant change. The rates quoted in this article are accurate as of January 16th, 2026, and are subject to change without notice.

Read the Full Fortune Article at:

https://fortune.com/article/current-mortgage-rates-01-16-2026/

[ Fri, Feb 20th ]: Fortune

[ Thu, Feb 19th ]: wjla

[ Wed, Feb 18th ]: Newsweek

[ Tue, Feb 10th ]: KOIN

[ Tue, Feb 10th ]: Fortune

[ Mon, Feb 09th ]: Fortune

[ Fri, Feb 06th ]: Fortune

[ Fri, Feb 06th ]: HousingWire

[ Fri, Feb 06th ]: Fortune

[ Tue, Feb 03rd ]: Fortune

[ Mon, Feb 02nd ]: Fortune

[ Mon, Jan 12th ]: Fortune