[ Mon, Feb 16th ]: Fox 5 NY

[ Mon, Feb 16th ]: Barron's

[ Mon, Feb 16th ]: Palm Beach Post

[ Mon, Feb 16th ]: Source New Mexico

[ Mon, Feb 16th ]: Daily Mail

[ Mon, Feb 16th ]: WTVD

[ Mon, Feb 16th ]: WXYZ

[ Mon, Feb 16th ]: London Evening Standard

[ Mon, Feb 16th ]: WDAF

[ Mon, Feb 16th ]: Chicago Sun-Times

[ Mon, Feb 16th ]: Associated Press

[ Mon, Feb 16th ]: Cleveland

[ Mon, Feb 16th ]: WTVF

[ Mon, Feb 16th ]: Deadline

[ Mon, Feb 16th ]: NBC New York

[ Mon, Feb 16th ]: KUTV

[ Mon, Feb 16th ]: WTOP News

[ Mon, Feb 16th ]: IBTimes UK

[ Mon, Feb 16th ]: CBS News

[ Mon, Feb 16th ]: People

[ Mon, Feb 16th ]: New York Post

[ Mon, Feb 16th ]: The Irish News

[ Mon, Feb 16th ]: syracuse.com

[ Mon, Feb 16th ]: WSB-TV

[ Mon, Feb 16th ]: NBC Los Angeles

[ Mon, Feb 16th ]: Toronto Star

[ Mon, Feb 16th ]: Local 12 WKRC Cincinnati

[ Mon, Feb 16th ]: WJTV Jackson

[ Mon, Feb 16th ]: Irish Examiner

[ Mon, Feb 16th ]: South Bend Tribune

[ Mon, Feb 16th ]: Newsweek

[ Mon, Feb 16th ]: The Jerusalem Post Blogs

[ Mon, Feb 16th ]: The Advocate

[ Mon, Feb 16th ]: Fortune

[ Mon, Feb 16th ]: Sports Illustrated

[ Mon, Feb 16th ]: TheWrap

[ Mon, Feb 16th ]: The Boston Globe

[ Mon, Feb 16th ]: Variety

[ Mon, Feb 16th ]: Orange County Register

[ Mon, Feb 16th ]: Government Executive

[ Mon, Feb 16th ]: Lehigh Valley Live

[ Mon, Feb 16th ]: BBC

[ Mon, Feb 16th ]: TheHockey Writers

[ Mon, Feb 16th ]: montanarightnow

[ Mon, Feb 16th ]: Heavy.com

[ Mon, Feb 16th ]: Townhall

[ Mon, Feb 16th ]: NPR

[ Mon, Feb 16th ]: Fox News

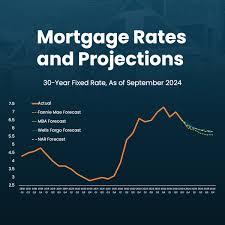

Mortgage Rates Fall to 4.5%

Fortune

FortuneLocale: UNITED STATES

Monday, February 16th, 2026 - Mortgage rates have continued their downward trajectory this week, offering a glimmer of hope for potential homebuyers and homeowners looking to refinance. The latest data from Freddie Mac indicates the average 30-year fixed-rate mortgage now sits at 4.5%, a notable drop from the 4.7% reported last week, and a significant decrease from the peak rates seen in late 2024. This ongoing decline is prompting increased activity in the housing market, though challenges remain.

The Shifting Landscape: A Deeper Dive into Rate Declines

The recent dip isn't a sudden occurrence; it's part of a gradual easing of rates that began in late 2025. Several interwoven economic factors are at play. Primarily, the Federal Reserve's monetary policy remains the key driver. After a series of aggressive rate hikes aimed at curbing inflation in 2023 and 2024, the Fed signaled a potential pause - and now, whispers of potential cuts - in early 2026, stemming from easing inflationary pressures and a stabilizing labor market. This shift in tone has had a cascading effect on various interest-sensitive sectors, with mortgage rates being particularly responsive.

Beyond the Fed, broader economic indicators are also contributing. A slowing but still resilient economy suggests reduced demand for borrowing, further alleviating pressure on rates. The yield on the 10-year Treasury bond, often used as a benchmark for mortgage rates, has also fallen, indicating investor confidence in a more moderate economic outlook. The relative stability of global markets, after periods of geopolitical uncertainty, has further contributed to this downward trend.

Refinancing: A Viable Option for Many, But Not All

The falling rates naturally lead to the question: should you refinance? For homeowners who secured mortgages at higher rates in recent years, the potential savings can be substantial. Even a seemingly small reduction - like moving from 6% to 4.5% - can translate to significant savings over the remaining life of the loan. Tools and calculators are readily available online to help homeowners estimate potential savings based on their specific loan balance, remaining term, and the difference in interest rates.

However, refinancing isn't a guaranteed win. Borrowers must carefully weigh the benefits against the costs. Closing costs, including appraisal fees, title insurance, and origination fees, can range from 2% to 5% of the loan amount. It's crucial to calculate the "break-even point" - the time it will take to recoup these costs through monthly savings - to determine if refinancing makes financial sense. Furthermore, extending the loan term through refinancing, while reducing monthly payments, will ultimately result in paying more interest over the life of the loan.

Beyond Refinancing: Opportunities for Buyers and the Overall Market

The decline in mortgage rates isn't just benefiting existing homeowners. It's also providing a much-needed boost to the housing market, increasing affordability for potential buyers. While inventory remains tight in many areas, lower rates are encouraging more people to enter the market, leading to increased competition and potentially moderating price growth. This is especially positive news for first-time homebuyers who have been priced out in recent years.

What Should Borrowers Do Now? A Checklist

- Shop Around: Don't settle for the first offer. Obtain quotes from multiple lenders - banks, credit unions, and online mortgage providers - to compare rates and fees. Utilize online comparison tools, but also speak directly with loan officers to discuss your specific situation.

- Understand Total Costs: Don't just focus on the interest rate. Carefully examine all closing costs and factor them into your calculations. Ask lenders for a detailed Loan Estimate to compare offers accurately.

- Assess Your Long-Term Plans: How long do you plan to stay in your home? If you anticipate moving within a few years, the benefits of refinancing may be outweighed by the closing costs.

- Check Your Credit Score: A higher credit score typically translates to a lower interest rate. Review your credit report for any errors and take steps to improve your score before applying for a loan.

- Consider Rate Lock Options: Once you find a favorable rate, explore rate lock options to protect yourself from potential increases while your loan is being processed.

Looking Ahead: What's on the Horizon?

While the current trend is encouraging, experts caution against complacency. The economic outlook remains uncertain, and unforeseen events could quickly reverse the downward momentum. The Federal Reserve's next moves will be crucial in shaping the future of mortgage rates. Many analysts predict rates will stabilize in the coming months, but a significant drop back to pre-pandemic levels appears unlikely. Homeowners and prospective buyers should remain vigilant, stay informed, and make informed decisions based on their individual financial circumstances.

Read the Full Fortune Article at:

[ https://fortune.com/article/current-refi-mortgage-rates-02-16-2026/ ]

[ Tue, Feb 10th ]: KOIN

[ Tue, Feb 10th ]: Fortune

[ Mon, Feb 09th ]: Fortune

[ Mon, Feb 09th ]: Fortune

[ Fri, Feb 06th ]: Fortune

[ Fri, Feb 06th ]: HousingWire

[ Fri, Feb 06th ]: Fortune

[ Tue, Feb 03rd ]: CNN

[ Tue, Feb 03rd ]: Fortune

[ Mon, Feb 02nd ]: Fortune

[ Mon, Feb 02nd ]: WSFA

[ Mon, Feb 02nd ]: Fortune