Waiting for a Housing Crash Costs You Money

- 🞛 This publication is a summary or evaluation of another publication

- 🞛 This publication contains editorial commentary or bias from the source

Why Waiting for a Housing Crash Is Costing You Money – A Quick Guide

The housing market has been a topic of heated debate for years, especially in the wake of the COVID‑19 pandemic, soaring mortgage rates, and the chatter that a “crash” is just around the corner. The Investopedia article “Why Waiting for the Housing Crash Is Costing You Money” takes a deep dive into why the idea of holding off on a purchase can be a costly gamble. Below is a concise summary of the main arguments, data, and practical take‑aways for anyone trying to decide whether to buy now, wait, or rent.

1. The Current Landscape: Prices, Rates, and Demand

Mortgage Rates Are Still Low Compared to Historical Peaks

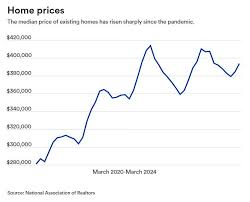

In the last year, the average 30‑year fixed‑rate mortgage hovered around 6–7 %, well below the 7‑8 % highs seen in 2021‑22. Even with recent upticks, those rates are comfortably below the long‑term average of 8.5 % that spanned the 1990s and early 2000s. In other words, borrowing costs remain relatively inexpensive for many buyers.Home Prices Are Rising, but Not All‑Out

According to data cited in the article (e.g., Zillow, Freddie Mac), the U.S. home‑price index is up about 14 % year‑over‑year, but the gains are uneven. Some markets have cooled while others (particularly in the Sun Belt and Midwest) remain hot. The overall trend still points to appreciation rather than a dramatic crash.Inventory Shortages Keep Demand High

The supply of homes for sale is at a record low. The article cites the National Association of Realtors (NAR) and the U.S. Census Bureau, noting that the inventory level is roughly 1.3 months of supply—well below the 3‑month benchmark for a balanced market. This scarcity keeps buyers in a competitive position.

2. The Cost of Waiting: Opportunity Cost, Rent, and Market Timing

Rent‑to‑Buy Cost Analysis

The article walks through a typical rent‑to‑buy calculation: If you’re renting a $1,500/month unit, you’re paying $18,000 annually. That money is not building equity and can be better invested. In many cities, rent has outpaced home‑price growth, meaning that buying sooner may lock in a lower cost per square foot.Opportunity Cost of Not Building Equity

Homeownership builds equity with each mortgage payment. The article uses a simple illustration: Buying a $300,000 home at a 3 % interest rate and 30‑year term means about $1,200/month. Over five years, the equity accumulated could exceed $20,000, assuming a modest 3‑5 % annual appreciation. That’s a return you lose if you keep renting.Timing the Market is Risky

While analysts predict that a sharp crash is unlikely, the article points out that past “crashes” (e.g., the 2008 housing crisis) took years to recover. By the time a crash materializes, many borrowers have already paid down significant portions of their loans and built equity. Waiting could mean missing the window for price appreciation and paying higher rates for a longer time.

3. Data-Driven Signals That a Crash Is Not Imminent

Economic Indicators

The article references the Federal Reserve’s stance on interest rates, the current unemployment rate, and the Consumer Price Index (CPI). It highlights that the economy is still solidly above the 2 % inflation target and that the labor market remains robust—conditions that typically support housing demand.Historical Comparisons

By comparing current price‑to‑income ratios (around 4.5‑5.0 in many markets) to historical peaks (7‑8 % pre‑2008), the article argues that the market is not yet at a “bubble” level. A true crash would require a massive correction in these ratios, which is currently considered unlikely.Expert Opinions

The piece quotes real‑estate analysts who warn against the “wait‑and‑see” mentality. A real‑estate strategist from a major brokerage firm noted that even if rates rise to 7‑8 %, the market would likely adapt rather than collapse.

4. Practical Advice for Buyers, Renters, and Investors

For Buyers: Secure a Low Rate Now

Lock in a mortgage rate as soon as possible, especially if you qualify for a fixed‑rate loan. The article emphasizes the benefit of a lower interest rate outweighing the potential of a future price drop.For Renters: Build a Plan to Transition

Renters should consider saving a down‑payment while keeping a flexible approach. If market conditions look favorable, a short‑term rental can be a cost‑effective bridge.For Investors: Diversify and Hedge

The article suggests that investors can hedge the risk by investing in a diversified portfolio that includes real‑estate‑related assets (REITs, mortgage‑backed securities). This strategy allows them to capture housing market upside without taking on direct property risk.

5. Bottom Line: Why Waiting Is a Mistake

Equity Creation vs. Rent Loss

The core argument is that by not purchasing, you give up the chance to create wealth through equity while continuing to pay rent that provides no return. Even if the market dips slightly, the long‑term appreciation and tax advantages still yield a net benefit.Low Risk of a Crash and High Cost of Waiting

The article makes a clear case that a crash is not only improbable in the short term but would come with a slow recovery, meaning the opportunity cost of waiting is significant. The long‑term trajectory of home prices continues to trend upward in most regions.Timing Is Not the Only Variable

Timing the market precisely is nearly impossible, but buying a home that fits your needs, budget, and location preferences remains a sound strategy. The article recommends focusing on fundamentals—price relative to income, neighborhood trends, and the ability to afford a mortgage—rather than chasing an elusive market bottom.

Takeaway: While a dramatic housing crash remains unlikely in the near future, waiting for one is a costly strategy. Renters risk losing money that could be invested elsewhere, and potential buyers miss out on building equity and capturing the continuing upward momentum of most U.S. housing markets. The article urges readers to weigh the long‑term benefits of ownership against the short‑term costs of waiting, suggesting that securing a mortgage and buying sooner is often the smarter financial decision.

Read the Full Investopedia Article at:

[ https://www.investopedia.com/why-waiting-for-the-housing-crash-is-costing-you-money-11781312 ]